TLDR

- AML compliance failures can trigger penalties in the billions — TD Bank faced $3.09 billion in combined fines in 2024 alone

- Federal regulations require banks, credit unions, broker-dealers, and MSBs to designate a qualified BSA/AML compliance officer

- CAMS certification is the industry benchmark; senior roles typically require 5+ years of direct program management experience

- Screen for risk judgment and regulatory adaptability, not just credentials — the role demands both

- Specialist recruiters significantly outperform generalist approaches when sourcing passive AML talent

What Does an AML Compliance Officer Do?

The AML compliance officer is responsible for designing, running, and continuously improving a financial institution's anti-money laundering program. The role goes well beyond general compliance work, sitting at the intersection of internal controls, regulatory reporting, and financial crime detection.

According to the FFIEC BSA/AML Examination Manual, the designated BSA compliance officer must be "responsible for coordinating and monitoring day-to-day BSA/AML compliance" and must hold the authority, independence, and competence to execute all duties effectively. Simply appointing someone to the title isn't enough. Regulators assess whether the individual is genuinely empowered to act.

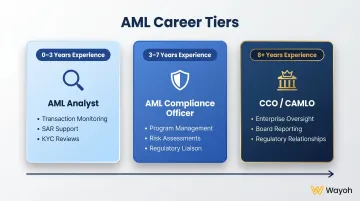

Role Levels Hiring Managers Should Distinguish

Before posting a job description, clarify which level your institution actually needs:

| Level | Typical Scope | Experience Range |

|---|---|---|

| AML Analyst | Transaction monitoring, SAR support, KYC reviews | 0–3 years |

| AML Compliance Officer | Program management, risk assessments, regulatory liaison | 3–7 years |

| CCO / CAMLO | Enterprise-wide oversight, board reporting, regulatory relationships | 8+ years |

These distinctions matter more than most hiring managers expect. At smaller institutions, one person may hold the BSA officer function under a CCO title. At global banks, a Chief Anti-Money Laundering Officer (CAMLO) may lead dozens of specialists. The regulatory obligation is identical in structure; what changes is the scale and complexity of execution.

Core Responsibilities of an AML Compliance Officer

Developing and Maintaining the AML Program

The AML officer owns the institution's entire BSA/AML compliance program — policies, internal controls, procedures, and the ongoing updates required as regulations evolve. This includes alignment with the Bank Secrecy Act, the USA PATRIOT Act, and FinCEN guidance under 31 CFR Chapter X.

The program requires continuous maintenance. FinCEN's proposed rule from April 2026 moves toward effectiveness-based compliance — meaning AML officers must now demonstrate that programs work, not just that paperwork was filed.

Conducting Risk Assessments

AML officers conduct regular risk assessments across customers, products, services, and geographic exposure. These assessments determine where the compliance program allocates resources — and they must reflect the institution's actual risk appetite, not a generic template.

A fintech processing high-volume cross-border payments faces materially different risks than a community bank. The officer's assessment methodology needs to match the environment.

Transaction Monitoring and Suspicious Activity Reporting

AML officers oversee transaction monitoring systems, investigate flagged activity, and file Suspicious Activity Reports (SARs) with FinCEN when warranted.

SAR volumes hit a record 4.105 million filings in 2025 — a 7.99% increase over 2024. Banks and credit unions alone filed more than 2.193 million. The workload is growing, and the consequences of failure are severe.

FinCEN assessed a $1 million personal civil penalty against Thomas Haider, a former Chief Compliance Officer, for BSA violations. A federal court confirmed that "willful" violations include reckless disregard — not just deliberate wrongdoing. The institutional penalties are even larger: Capital One paid $390 million in 2021 for failing to file thousands of SARs and CTRs.

Customer Due Diligence (KYC/CDD)

AML officers implement Know Your Customer and Customer Due Diligence procedures — verifying identities, assigning risk ratings, and applying enhanced due diligence to high-risk accounts. Under FinCEN's CDD Final Rule, this includes identifying beneficial owners of legal entities at a 25% ownership threshold.

This function connects directly to onboarding workflows. The AML officer must work closely with operations and product teams — not just the compliance department.

Training, Reporting, and Internal Communication

The AML officer trains all staff on AML obligations, reports compliance status to the board and senior management, and serves as the institution's primary liaison with regulators and external auditors.

One critical point hiring managers often underestimate: the officer must hold sufficient authority — typically at director level or above — to challenge business decisions and escalate concerns without being overridden. Authority on paper isn't enough if the culture doesn't support it.

Required Qualifications and Certifications

Education and Experience Benchmarks

- Entry-level to officer roles: Bachelor's degree in finance, accounting, law, economics, or a related field

- Senior roles (CCO, CAMLO): MBA, JD, or CPA often preferred; law enforcement or banking regulatory experience can substitute at the senior or executive level

- Experience minimum: Most institutions expect 3–5 years of direct compliance experience for officer-level hires; senior roles require program management and direct regulatory engagement

- Fintech roles: Hands-on experience with risk systems and compliance technology may outweigh a traditional banking background

These thresholds set the baseline. Certifications are where you separate candidates who understand AML conceptually from those who've committed to it professionally.

Certifications to Require or Prefer

| Certification | Issuing Body | Signal to Employer |

|---|---|---|

| CAMS (Certified Anti-Money Laundering Specialist) | ACAMS | Industry-standard AML credential; 120-question exam, 3-year recertification |

| CRCM (Certified Regulatory Compliance Manager) | ABA | Depth in U.S. banking regulatory compliance; valued at banks and credit unions |

| CFCS (Certified Financial Crime Specialist) | ACFCS | Broader financial crime scope — AML, fraud, anti-corruption, cyber |

| CAFP (Certified AML and Fraud Professional) | ACAMS | Integrated AML/fraud function experience |

CAMS is the benchmark. Any officer-level candidate who doesn't hold it should have a compelling reason and a clear timeline to earn it.

Critical Skills Financial Firms Should Screen For

Regulatory Knowledge and Adaptability

Candidates must demonstrate fluency with the BSA, USA PATRIOT Act, FinCEN guidance, and FATF Recommendations. More important than recitation: ask how they've responded to regulatory change in prior roles. The April 2026 FinCEN reform proposal makes adaptability non-negotiable — static compliance expertise has a short shelf life.

Analytical and Investigative Ability

AML officers analyze large transaction datasets, identify anomalies, and connect disparate data points into a coherent picture of potential illicit activity. Credentials don't prove this skill — include a practical scenario or case exercise in your interview process to assess it.

Risk Management Judgment

Strong AML officers assess the institution's specific risk profile, prioritize resources accordingly, and make defensible decisions under ambiguity. At fintech firms — where risk exposure shifts rapidly with new products or markets — that judgment separates candidates who can keep pace from those who can't.

Communication and Stakeholder Management

AML officers explain complex findings to frontline staff, senior leadership, board members, and regulators. Assess written communication through SAR narrative samples or policy memo drafts. Verbal communication through scenario-based interviews — not just behavioral questions.

Technological Proficiency

Compliance technology proficiency is now a baseline requirement. Expect candidates to have hands-on experience with:

- Transaction monitoring platforms

- KYC/CDD and sanctions screening tools

- Case management systems

- For fintechs specifically: API-driven compliance infrastructure and data analytics tools

When Should Your Firm Hire a Dedicated AML Compliance Officer?

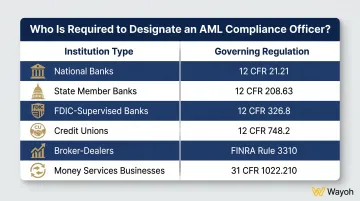

Regulatory Mandates by Institution Type

The short answer: most covered institutions are already legally required to designate one.

| Institution Type | Governing Regulation |

|---|---|

| National banks | 12 CFR 21.21 (OCC) |

| State member banks | 12 CFR 208.63 (Federal Reserve) |

| FDIC-supervised banks | 12 CFR 326.8 (FDIC) |

| Credit unions | 12 CFR 748.2 (NCUA) |

| Broker-dealers | FINRA Rule 3310 |

| Money Services Businesses | 31 CFR 1022.210 |

Broker-dealers face an additional requirement under FINRA Rule 3310: the AML compliance officer must be an associated person of the firm, and their contact information must be registered directly with FINRA.

Fintechs operating as MSBs — money transmitters, check cashers, currency dealers — must register with FinCEN and designate a compliance officer under 31 CFR 1022.210.

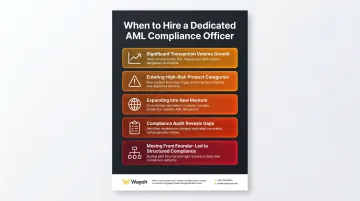

Operational and Growth Triggers

Beyond the regulatory floor, firms should move proactively when:

- Transaction volume scales significantly

- Entering high-risk product categories (crypto, cross-border payments, lending)

- Expanding into new markets with distinct regulatory exposure

- A compliance audit reveals gaps a generalist cannot address

- The firm moves from founder-led compliance to structured accountability

Delaying the hire compounds risk: each quarter without qualified oversight adds potential SAR failures, program gaps, and examiner findings to the ledger.

Firms unsure whether they need a senior officer, a junior analyst, or a fractional arrangement often find that an interim hire is the right first step — it covers the regulatory gap while the firm defines the permanent role. Wayoh has placed compliance professionals in exactly these situations across banks, fintechs, and other regulated institutions, and can help structure the right engagement from the start.

How to Recruit the Right AML Compliance Officer

Write a Job Description That Reflects the Role

Generic compliance postings don't attract qualified AML specialists — they attract generalists who fit the keywords. An effective posting should specify:

- Required certifications (CAMS minimum; CRCM or CFCS preferred)

- The regulatory frameworks the officer will operate within

- The institution's risk profile and product/service categories

- Reporting structure and the level of authority the role holds

- Whether the role includes direct regulatory interaction

Vague postings signal a firm that doesn't fully understand what it's hiring for. That deters the candidates you most want.

Screen for Regulatory Fit, Not Just Credentials

CAMS certification confirms baseline knowledge. What it can't tell you is whether the candidate's experience actually matches your regulatory environment. A community bank BSA officer and a neobank compliance lead may hold identical credentials while operating in completely different worlds.

Develop interview questions around your firm's actual risk exposure — specific products, customer segments, geographic footprint, and prior examiner findings. Ask what they would change about your current program in the first 90 days.

Verify Integrity Under Pressure

AML officers handle sensitive financial data and hold reporting obligations that can put them at odds with commercial interests. Background checks are a starting point, not a finish line.

Reference checks should explicitly probe how candidates behaved when business pressure conflicted with compliance requirements. Regulatory "fit and proper" standards are a useful benchmark — the question isn't just whether someone is competent, but whether they'll act on what they know.

Assess Authority Dynamics Honestly

Integrity under pressure only matters if the role carries real authority. Before extending an offer, assess honestly whether your organization supports that authority. An AML officer who cannot push back on a business decision or escalate directly to the board is an officer in title only, and regulators will treat the institution accordingly.

Ask candidates directly: describe a situation where you had to challenge a senior decision on compliance grounds. What happened? Their answer tells you whether they've operated with real authority — and whether your firm's culture can support that.

Partner with a Specialist Recruiter

General recruiters rarely maintain the compliance-specific networks or regulatory knowledge required to source and vet AML talent effectively. The talent gap in AML hiring is well-documented — qualified passive candidates don't surface through job boards.

Wayoh focuses exclusively on compliance, risk, and legal hiring across major U.S. markets. With over a decade in regulated-industry recruitment and 500+ placements, the firm delivers pre-vetted candidates who meet both technical and regulatory requirements — reducing time-to-hire and the cost of a mis-hire that typically exceeds the placement fee.

Frequently Asked Questions

What does an AML compliance officer do?

An AML compliance officer designs and enforces a financial institution's anti-money laundering program — overseeing transaction monitoring, conducting risk assessments, managing KYC/CDD procedures, and reporting suspicious activity to FinCEN via SARs. They serve as the primary regulatory liaison on financial crime matters.

What are the main responsibilities of an AML compliance officer?

Core responsibilities include developing AML policies, conducting risk assessments, monitoring transactions, filing SARs with FinCEN, and training staff on BSA/AML obligations. The role also carries direct reporting duties to senior management and the board.

What are the main pillars of AML/KYC compliance?

The core pillars are customer due diligence (CDD/KYC), transaction monitoring, suspicious activity reporting (SARs), risk-based internal controls, and ongoing staff training. These align with the BSA's four minimum program requirements: internal controls, independent testing, a designated BSA officer, and training.

What degree or qualifications do you need to work in AML?

A bachelor's degree in finance, accounting, law, or a related field is standard. The CAMS certification from ACAMS is widely considered the industry benchmark. Senior roles often require an MBA, JD, or CPA designation alongside 5+ years of direct compliance experience.

What skills are needed for AML compliance officers?

Critical skill areas include deep regulatory knowledge, analytical and investigative ability, sound risk judgment, clear communication across diverse stakeholders, and proficiency with transaction monitoring and KYC technology platforms.

How much is an AML compliance officer paid?

The BLS reports a median of $78,420 for compliance officers broadly, while Robert Half benchmarks the range at $90,000–$132,000 for experienced compliance officers. AML-specific roles average approximately $98,949 according to ZipRecruiter, with senior CCO-level roles reaching $155,000–$200,000. Compensation varies by institution type, geographic market, and whether the candidate holds CAMS certification.