Introduction

Regulatory enforcement isn't slowing down. In 2024 alone, TD Bank paid $1.3 billion — the largest FinCEN penalty ever levied against a depository institution — for systemic failures in its AML program. OKX followed in 2025 with a $504 million settlement. Inadequate AML staffing is an existential risk, not just a compliance gap.

That enforcement pressure is driving demand for qualified AML professionals — but supply hasn't kept up. Regulatory scope keeps expanding, while the pool of certified, experienced candidates remains tight.

This guide is written for compliance leaders and HR teams actively building or strengthening AML functions at banks and fintechs across the U.S. It covers:

- The roles you need to hire and what each one actually does

- The qualifications and certifications that carry real weight

- How hiring differs between banks and fintechs

- How to attract top AML talent in a tight, competitive market

TL;DR

- Regulatory enforcement is tightening — banks, fintechs, and crypto-adjacent firms are under pressure to staff AML functions fast

- Most in-demand roles: BSA/AML Officers, KYC/CDD Analysts, SAR Investigators, and Sanctions Compliance Specialists

- CAMS from ACAMS is the gold-standard credential — prioritize it for leadership and senior individual contributor roles

- Banks and fintechs have fundamentally different hiring needs — fintechs need builders, banks need operators with exam experience

- A specialized AML recruiter shortens time-to-hire and surfaces vetted candidates that generalist searches miss

The Growing Demand for AML Compliance Professionals

Enforcement Is Getting Expensive

U.S. regulators have made clear that AML program failures carry severe financial consequences. Recent major enforcement actions include:

| Year | Entity | Penalty | Primary Violation |

|---|---|---|---|

| 2023 | Binance | $4 billion+ | BSA violations, unregistered MSB |

| 2024 | TD Bank | $1.3 billion | Inadequate AML program, SAR failures |

| 2025 | OKX | $504 million | Unlicensed money transmitter |

| 2025 | KuCoin | $297 million | Failing AML/KYC programs |

Each of these cases involved understaffed or under-resourced compliance functions. FinCEN recorded 4.8 million SARs filed in FY 2024, with depository institutions alone filing 2.1 million. That volume requires trained people — and institutions that cut corners on headcount pay for it later.

A Real Talent Shortage

Those enforcement costs make the talent shortage a direct business risk — not just an HR problem. According to a 2023 ACAMS survey, 42% of AML professionals have considered leaving their roles, while 68% report high stress levels. On the demand side, over 2,300 BSA/AML positions are actively posted on Indeed at any given time.

Three structural factors drive the gap:

- Regulatory expansion — The Anti-Money Laundering Act of 2020 extended BSA obligations to fintechs, money service businesses, and crypto exchanges, sharply expanding the employer base competing for the same certified talent

- Limited certification pipeline — CAMS requires time and experience to earn; you can't manufacture qualified AML professionals on demand

- Fintech growth — 70% of fintech leaders cite talent shortage as their biggest barrier to growth, with compliance hiring a primary bottleneck

The result: banks and fintechs are competing for the same constrained pool — and most are hiring at the same time.

Key AML Roles Banks and Fintechs Need to Hire

BSA/AML Compliance Officer

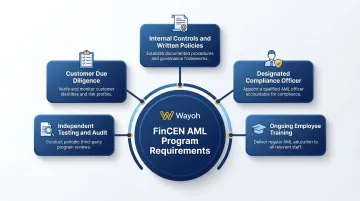

This is the cornerstone hire. Under 31 U.S.C. 5318(h) and 31 CFR Part 1020, every financial institution must designate a BSA/AML Compliance Officer — there is no asset threshold exemption. This person owns the entire AML program and is accountable for all five pillars required by FinCEN:

- Internal controls and written policies

- Designation as the compliance officer

- Ongoing employee training

- Independent testing and audit

- Customer due diligence (added as a formal pillar under the 2016 CDD Final Rule)

At banks, this person also manages examiner relationships and ensures the program survives regulatory scrutiny. At fintechs, they often build the program from scratch.

KYC and Customer Due Diligence Analysts

KYC/CDD Analysts are the highest-volume compliance hire, particularly at fintechs onboarding large customer populations. Their core responsibilities include:

- Identity verification and document review

- Beneficial ownership checks (per the CDD Final Rule, any individual owning 25% or more of a legal entity)

- Customer risk profile development

- Ongoing transaction monitoring and relationship reviews

Demand for KYC talent spiked when FinCEN's CDD Final Rule took effect in May 2018 and has remained elevated as digital onboarding volume continues to grow.

AML Investigators and SAR Filers

AML investigators review flagged transaction alerts, conduct case analysis, and file Suspicious Activity Reports with FinCEN, typically within 30 calendar days of detection. Continuing suspicious activity requires follow-up SARs every 90 days.

The role demands both investigative instincts and precise documentation skills. A poorly written SAR narrative can create regulatory liability even when the underlying filing is timely.

Sanctions Compliance Specialists

Sanctions is a distinct but adjacent function, and demand has intensified since Russia's invasion of Ukraine. OFAC designated nearly 500 individuals and entities in February 2024 alone, with eight separate announcements adding 100+ SDN list entries throughout the year.

Sanctions specialists need direct experience with:

- SDN list and OFAC sanctions program screening

- Automated screening tools and exception escalation

- UN and EU sanctions list requirements for institutions with international exposure

AML Technology and Data Roles

75% of banks now use machine learning in case management and investigations, making AML technology the fastest-growing hiring category in financial crime compliance. Institutions need professionals who can actively work with these systems, not just receive their alerts.

In-demand roles include:

- Transaction monitoring system administrators (NICE Actimize, Oracle FCCM, Verafin)

- AML data analysts and model validators

- AI/ML tuning specialists who can reduce false positives at scale

These professionals are the scarcest in the market and command premium compensation. The global AML software market is projected to grow from $4.13 billion in 2025 to $9.38 billion by 2030. The talent to operate these systems needs to scale alongside that growth.

What to Look for in an AML Compliance Candidate

Certifications That Signal Readiness

CAMS (Certified Anti-Money Laundering Specialist) from ACAMS is the primary credential. With 120,000+ members across 200+ countries, it's recognized by regulators, financial institutions, and governments across 200+ countries as the benchmark for AML competency. For leadership roles, it should be treated as a near-requirement.

Two secondary credentials worth recognizing:

- CFCS (Certified Financial Crime Specialist) — Broader than CAMS, covering 12 areas including fraud, cyber, and terrorist financing. Useful for investigators working across financial crime types

- CRCM (Certified Regulatory Compliance Manager) — Bank-focused credential from the ABA; requires 3 years of U.S. compliance experience. Strong signal for candidates moving into regulatory compliance management roles

ACAMS also offers specialist credentials in sanctions (CGSS) and crypto (CCAS) — relevant for fintech hiring.

Regulatory and Technical Knowledge

Bank hires — look for working knowledge of:

- BSA and USA PATRIOT Act requirements

- FinCEN regulations

- Primary regulator frameworks (OCC, FDIC, or Federal Reserve)

Fintech hires — add:

- CFPB guidance

- State money transmitter license requirements

- FinCEN's CVC guidance on convertible virtual currencies

Transaction Monitoring System Experience

Candidates with hands-on system experience are significantly more valuable than those with only theoretical knowledge. Specifically look for:

- Direct experience tuning detection rules in Actimize, Oracle FCCM, or Verafin

- Track record of reducing false positive rates at scale

- Experience managing alert queue volume (especially relevant for high-volume fintechs)

Investigative Soft Skills

A resume won't surface these — structured behavioral interviews will:

- Ability to write clear, defensible SAR narratives

- Sound judgment in ambiguous, time-pressured situations

- Attention to detail across high-volume caseloads

- Comfort operating in a regulated environment with strict deadlines

Institution-Type Match

Weight prior experience at comparable institution types. A community bank candidate may lack the volume or regulatory complexity exposure needed at a Tier 1 bank. Conversely, a large-bank candidate may struggle with the ambiguity and generalist scope expected at an early-stage fintech.

Ask directly: what did their prior program look like, who did they report to, and what did a typical week involve?

AML Hiring: Banks vs. Fintechs

How Banks Hire for AML

Traditional bank AML hiring tends to be:

- Requires sign-off from legal, HR, and senior leadership — multi-stage processes that move deliberately

- Favors candidates with direct regulatory exam exposure and documented program ownership

- Defines role scope tightly — a KYC analyst handles KYC; SAR review lives elsewhere on the team

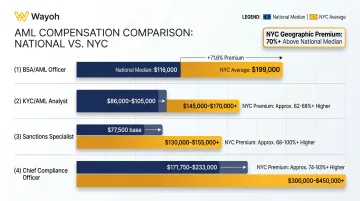

Banks offer higher base salaries. BSA/AML Officers earn a national median of approximately $116,000, with roles in New York City averaging approximately $199,000 — a geographic premium exceeding 70%.

How Fintechs Hire for AML

Where banks prize specialization and process, fintechs demand range and speed:

- Covers multiple functions at once — a single compliance hire at a Series B may own KYC, SAR review, and sanctions screening

- Requires program-building experience — many fintechs are constructing AML frameworks from scratch, not maintaining established ones

- Moves faster — prolonged searches create real regulatory exposure during growth phases, so open roles rarely stay open long

The regulatory risk at early-stage fintechs is real. A candidate who can only maintain an existing program won't survive in an environment where the program itself is still being written. Equity and remote flexibility often fill the gap where base salary can't compete with banks.

Compensation at a Glance

| Role | National Median | NYC Average | Notes |

|---|---|---|---|

| BSA/AML Officer | ~$116,000 | ~$199,000 | Significant geographic premium |

| KYC/AML Analyst | ~$86,000–$105,000 | Higher | Fintechs supplement with equity |

| Sanctions Specialist | ~$77,500 base | Higher | Demand increasing sharply post-2022 |

| Chief Compliance Officer | $171,750–$233,000 | Higher | Robert Half 2026 range |

How to Build and Scale Your AML Compliance Team

Permanent Core vs. Flexible Capacity

Effective AML teams combine two staffing layers:

Permanent core roles:

- BSA/AML Officer

- Senior investigators and program managers

- Sanctions leads and KYC program owners

Flexible capacity for volume-driven needs:

- KYC analysts during onboarding surges

- SAR review staff during remediation

- Transaction monitoring specialists for backlog clearance

Contract and interim AML staffing has become standard for regulatory remediation projects, product launches, and transaction volume spikes. Wayoh supports both permanent and interim AML placements for banks and fintechs across major U.S. markets — including New York, San Francisco, and Miami. All interim consultants are fully vetted through references and background checks before placement.

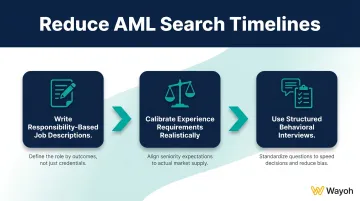

Reducing Time-to-Hire

Three practical adjustments that cut AML search timelines:

- Write job descriptions around actual responsibilities — not regulatory checkbox language. Specify the systems used, the filing volumes expected, and the regulatory relationships involved

- Calibrate experience requirements honestly — many analyst-level roles that list 5+ years of experience can be performed effectively by qualified 2–3 year candidates. Over-specification shrinks your pool without improving outcomes

- Use structured behavioral interviews — scenario-based questions that assess investigative judgment and SAR narrative quality tell you more than credential verification alone

The Case for a Specialized AML Recruiter

A bad compliance hire carries costs beyond salary. Regulatory exposure from an underqualified BSA Officer, or a delayed SAR program from an under-resourced investigative team, can dwarf the cost of the search.

A recruiter with deep AML market knowledge closes that gap in ways internal sourcing rarely can:

- Reaches experienced AML professionals who aren't on job boards and aren't actively looking

- Distinguishes a genuine CAMS holder from someone who listed it aspirationally

- Delivers faster shortlists through direct relationships, not keyword matching

Wayoh has spent 10+ years building those relationships across banking and fintech compliance — with 500+ placements in regulated industries to show for it.

Frequently Asked Questions

What is an AML compliance program?

An AML compliance program is the formal framework a financial institution implements to detect, prevent, and report money laundering. FinCEN requires it to include five pillars: a designated compliance officer, internal policies and controls, employee training, independent testing, and customer due diligence procedures.

What is AML KYC compliance?

KYC (Know Your Customer) is a core AML component requiring institutions to verify customer identities, understand the nature of their financial activity, and assess money laundering risk at onboarding and throughout the relationship.

What are the requirements for AML verification?

Institutions must collect and verify customer identifying information (name, address, date of birth, ID number), screen against OFAC sanctions lists, establish the purpose of the account, and conduct ongoing transaction monitoring. Beneficial ownership verification is required for legal entity customers under the CDD Final Rule.

What are the five main indicators of money laundering?

The most commonly cited red flags include:

- Structuring transactions to stay below reporting thresholds

- Rapid movement of funds through multiple accounts

- Use of cash-intensive businesses to obscure fund sources

- Significant inconsistencies between stated income and transaction volumes

- Ties to high-risk jurisdictions or sanctioned entities

What are examples of AML compliance in practice?

Common AML compliance activities include:

- KYC onboarding checks that verify customer identity

- Automated transaction monitoring systems that flag unusual activity

- SAR filings submitted to FinCEN within required deadlines

- Sanctions screening against OFAC's SDN list

- Enhanced due diligence reviews for high-risk account relationships