Introduction

Hiring a Chief Anti-Money Laundering Officer (CAMLO) is not a routine executive search. When FinCEN fined Michael LaFontaine $450,000 personally for BSA program failures at U.S. Bank — and Thomas Haider $1,000,000 for compliance officer misconduct — the message was unambiguous: AML leadership failures carry direct, personal consequences. Getting this hire wrong isn't just an operational problem — it's a liability.

That regulatory pressure compounds a real talent problem. 67% of financial services employers report difficulty finding skilled compliance talent — and the pool of candidates who combine senior AML leadership experience, regulatory fluency, and technology acumen is structurally limited.

What follows breaks down the role's real requirements, what separates strong candidates from credentialed ones, and where most institutions go wrong in the search process.

TL;DR

- CAMLO is a personal liability role — candidates and institutions both face real legal and regulatory exposure

- CAMS certification is the baseline credential; 10+ years in compliance with 3–5 years in senior AML leadership is the typical benchmark

- Most CAMLO searches take 3–6 months — top candidates are passive and won't surface through job postings

- Misaligned job descriptions and unrealistic timelines are the most common reasons searches fail

- Working with a specialized recruiter who holds an existing passive candidate network cuts time-to-hire

What Does a Chief AML Officer Do?

The CAMLO is the senior executive accountable for an institution's entire AML and counter-terrorist financing (CTF) program. The title varies — some institutions use BSA Compliance Officer, others CCO or MLRO — but per the FFIEC BSA/AML Examination Manual, what regulators actually examine is functional authority, not the label on the org chart.

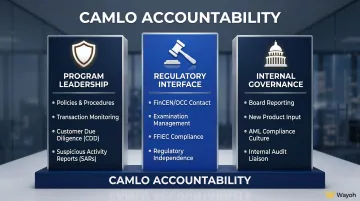

The Three Core Accountability Pillars

1. Program Leadership

- Developing AML policies, risk-based controls, and compliance frameworks

- Overseeing transaction monitoring, customer due diligence (CDD), SARs, and CTR filings

- Building and managing the compliance team

2. Regulatory Interface

- Serving as the primary point of contact with FinCEN, the OCC, and other regulators

- Managing the institution through examinations and enforcement inquiries

- Maintaining the independence and authority that FFIEC examiners specifically assess

3. Internal Governance

- Reporting directly to the board and C-suite on program performance, gaps, and emerging risk

- Providing input before the institution expands into new products, services, or geographies

- Ensuring compliance culture runs through the organization, not just the compliance department

Why Personal Liability Changes the Calculus

Most executive roles carry professional risk. CAMLO carries personal legal risk. FinCEN's enforcement action against LaFontaine wasn't against U.S. Bank alone — it was against him individually for maintaining improper alert caps despite explicit warnings. Haider's $1,000,000 penalty followed a 2016 federal court ruling that "willful" BSA violations include conduct marked by reckless disregard or willful blindness.

This liability profile has a direct effect on hiring:

- Strong candidates evaluate opportunities carefully before accepting them

- Institutions that can't demonstrate genuine board support and program resourcing will lose those candidates to competitors that can

The Technology Dimension

The 2018 Joint Statement on Innovation (FinCEN, OCC, Fed, FDIC, NCUA) and the AML Act of 2020 both explicitly encourage AI adoption in BSA/AML programs. Today's CAMLO candidates need fluency in transaction monitoring platforms, sanctions screening tools, and data analytics; regulatory knowledge alone is no longer sufficient. That broader skill requirement has narrowed an already thin talent pool.

Key Qualifications to Look for When Hiring a CAMLO

Education and Background

The baseline is a bachelor's degree in law, finance, accounting, or economics. Strong candidates typically hold a JD, MBA, or CPA and come from legal, regulatory, or investment banking backgrounds. Former bank examiners and OCC/FinCEN alumni are consistently among the strongest candidates.

Certifications That Signal Credibility

| Credential | Issuing Body | Relevance |

|---|---|---|

| CAMS | ACAMS | Global standard for AML expertise; 65,000+ certified professionals worldwide |

| CRCM | American Bankers Association | U.S. consumer banking compliance; useful for traditional bank CAMLOs |

| CRCP | FINRA | Securities-industry focused; narrower than CAMS for AML-specific roles |

CAMS is the benchmark. At large regulated institutions, it functions as a baseline filter, not a differentiator — the question is whether a candidate has it, not whether it's impressive that they do.

Certifications confirm technical grounding, but they don't tell you whether someone can run a program under regulatory pressure. That's where experience profile becomes the real filter.

Experience Profile

The qualifications that separate strong candidates from technically eligible ones:

- Program-building experience — not just maintaining an existing program, but actually designing or overhauling one

- Regulatory examination exposure — direct experience managing the institution through examinations or enforcement actions

- Team leadership — a track record managing compliance analysts, AML investigators, and second-line staff

- 10+ years in compliance, with at least 3–5 years in a senior AML leadership role

Soft Skills That Get Overlooked

CAMLOs spend as much time in the boardroom as the compliance department. The role requires:

- Converting regulatory risk into business language that resonates with non-compliance executives

- Managing relationships with regulators, auditors, law enforcement, and internal stakeholders simultaneously

- Able to challenge business lines constructively — without creating adversarial dynamics

None of this shows up on a resume. Structured behavioral interviews should probe for specific past situations — how a candidate handled an enforcement action, pushed back on a business unit, or briefed a board under pressure. Reference conversations with prior managers and regulators are equally important.

CAMLO vs. CCO vs. MLRO: Understanding Role Distinctions Before You Hire

Confusing these three roles before you write the job description wastes months and typically ends in a mis-hire.

CAMLO vs. CCO

The CCO manages enterprise-wide regulatory compliance — securities, consumer protection, data privacy, and more. The CAMLO is specifically accountable for financial crime risk and AML/CTF. These are not interchangeable.

FinCEN's FIN-2014-A007 advisory makes the compliance culture point clearly: a "financial institution with a poor culture of compliance is likely to have shortcomings in its BSA/AML program regardless of size." An AML program buried under an already-burdened CCO is a structural weakness examiners will find.

The FFIEC is explicit: the BSA compliance officer must operate "without undue influence from the bank's business lines." Assigning AML as a secondary function to a CCO managing multiple other regulatory domains directly contradicts this standard.

CAMLO vs. MLRO

The MLRO (Money Laundering Reporting Officer) is primarily a UK/EU regulatory construct with a narrower remit — focused on receiving and assessing internal suspicious transaction reports. A U.S. CAMLO carries broader programmatic responsibility across CDD, SAR filings, CTRs, risk assessment, and full program management.

For firms operating across jurisdictions, the functional scope — not the title — determines which role you actually need.

Before You Write the Job Description

Answer these questions before drafting the job description:

- Does AML sit inside a broader compliance function, or does it stand alone?

- What are the reporting lines — directly to the CEO and board, or through a CCO?

- What is the regulatory designation requirement for your charter type?

Firms that skip this step typically surface candidates built for the wrong scope — and discover the mismatch three months into a search.

The CAMLO Talent Market: Demand, Scarcity, and Compensation

Why This Market Is Tight

ACAMS reports 65,000+ CAMS-certified professionals globally. That sounds significant until you filter for U.S.-based, senior-level, with program-building experience and technology fluency. The working pool of realistic CAMLO candidates at any given time is much smaller than that number suggests.

Demand has accelerated in fintech and digital banking, where AML programs are being built from scratch and the need for experienced program architects — not just program maintainers — is acute. The Thomson Reuters 2023 Cost of Compliance survey found 73% of firms expect the cost of senior compliance staff to increase, which reflects this supply pressure.

Compensation Benchmarks

The BLS median for all compliance officers is $78,420 — but that figure covers entry-level through mid-level roles across all industries, and it doesn't describe the CAMLO market.

| Role | Approximate Range | Source |

|---|---|---|

| BSA/AML Officer | $89K–$151K total pay | Glassdoor (2026) |

| BSA/AML Officer (NYC) | Avg. $99,083 | ZipRecruiter (May 2026) |

| Chief AML Officer (U.S.) | Avg. ~$151,203 | ZipRecruiter (May 2026) |

CAMLO compensation at large national banks or major fintechs often exceeds these figures once bonuses and deferred compensation are added. New York and San Francisco command meaningful market premiums.

How Senior AML Executives Actually Move

Most CAMLO-level candidates are not actively job searching. They're not refreshing LinkedIn or applying through portals. They move through trusted referral networks and direct outreach from people they know and respect.

Firms that rely primarily on job postings will consistently underperform here. Top candidates evaluate opportunities on a short list of factors:

- Program maturity and institutional readiness

- Genuine board-level commitment to compliance

- Team quality and resource adequacy

- Evidence that the institution won't recreate the liability conditions they've spent careers avoiding

Common Mistakes Financial Firms Make When Recruiting a CAMLO

Writing the Wrong Job Description

Two failure modes show up repeatedly:

- Underselling the role — describing it as "Senior Compliance Manager" with a list of software tools, which tells serious CAMLO candidates the institution doesn't understand what they're actually hiring for

- Over-specifying technically — excluding strong strategic candidates who have the regulatory authority and leadership track record but don't tick every platform checkbox

The job description should lead with regulatory accountability, reporting structure, and program scope — not a bulleted list of transaction monitoring vendors.

Underestimating the Timeline

CAMLO searches in competitive markets realistically take 3–6 months. Industry data shows 8–12 weeks from shortlist to signed offer, combined with notice periods of 3–6 months at the C-suite level. That adds up to a vacancy window of 5–9 months — long enough to draw examiner scrutiny.

The FFIEC examination manual expects a designated, qualified BSA compliance officer in place with adequate resources. Examiners don't accept "we're still looking" as an answer. The TD Bank OCC consent order (2024) is a direct reminder that pursuing growth without a functioning BSA/AML program ends in enforcement action.

Underweighting Cultural Fit

Because AML is viewed as a technical function, hiring committees often optimize purely for credentials. That's the easier screen. The harder question is whether the candidate can influence executive leadership, push back on business lines without burning relationships, and actually build compliance culture — not just document it.

Those qualities are harder to assess in an interview, but they're what separates a two-year success from an 18-month exit. Budget time in the process to evaluate them directly.

How a Specialized Recruiter Accelerates Your CAMLO Search

A generalist executive search firm can source resumes. A compliance-specialized recruiter can evaluate whether the candidate who looks strong on paper has actually built an AML program, managed a regulatory examination, or navigated an enforcement inquiry — or simply maintained someone else's infrastructure without ever owning the outcomes.

The distinction matters for a role where a mis-hire creates regulatory and reputational risk, not just a personnel problem.

Wayoh Financial Services Recruiting has spent over 10 years placing compliance, risk, and legal professionals across banking, fintech, and healthtech, with 500+ professionals placed through a relationship-led model. For CAMLO-level searches specifically, that means direct access to senior AML executives who aren't visible on job boards, across major U.S. markets including New York, California, and Florida.

Wayoh also supports interim CAMLO placements for leadership gaps during permanent searches, regulatory remediation projects, or AML program buildouts. Every professional goes through full vetting and reference checks before a client introduction.

When evaluating a recruiting partner for this hire, look for:

- Demonstrable AML leadership placements (not just general compliance)

- Ability to articulate current market dynamics for this specific talent pool

- A structured process with regular updates and transparent timelines

- Access to passive candidates through genuine relationships, not database matching

Frequently Asked Questions

How much does an anti-money laundering officer make?

Compensation varies significantly by seniority. Mid-level BSA/AML Officers earn roughly $89K–$151K in total pay (Glassdoor, 2026), while Chief AML Officers average approximately $151,203 nationally (ZipRecruiter, May 2026). Large national banks and major fintechs in New York or San Francisco typically pay well above these figures once bonuses and deferred compensation are included.

What does a Chief AML Officer do?

The CAMLO leads the institution's full AML and CTF compliance program, serves as the primary regulatory contact during examinations, and reports directly to the board on financial crime risk. The role is fundamentally strategic — owning program design, team leadership, and regulatory relationships at the same time.

Is AML a difficult job?

Yes, by most measures. The role carries personal liability exposure, heavy regulatory accountability, high-stakes decision-making, and increasingly complex technology demands. For experienced professionals who understand the landscape, it is also among the most well-compensated and high-impact career paths in financial services compliance.

What certifications should a CAMLO have?

CAMS (Certified Anti-Money Laundering Specialist) is the most recognized and widely required credential — at large regulated institutions, it's typically a baseline requirement, not a differentiator. CRCM (Certified Regulatory Compliance Manager) is relevant for traditional bank roles, and CRCP applies more narrowly to securities-industry contexts.

How long does it typically take to hire a Chief AML Officer?

Plan for 3–6 months in competitive markets. Senior compliance searches average 8–12 weeks from shortlist to signed offer, and most CAMLO-level candidates carry notice periods of 3–6 months. Engaging a recruiter with an established passive candidate pipeline — rather than relying on active job postings — is the most effective way to compress that timeline.