The result: banks face a structural talent shortage at precisely the moment they can least afford one.

This article covers what risk management in banking actually requires — the core categories, the specialized roles, and the 2026 hiring landscape — plus a practical strategy for finding the qualified professionals your institution needs.

TLDR

- Banks face a genuine talent shortage, not a cyclical one : financial examiner roles are growing at 19% while the labor pipeline isn't keeping up

- Each of the six core risk categories requires distinct expertise; generalist coverage leaves real gaps

- The most in-demand roles in 2026: Chief Risk Officers, model risk analysts, AML/BSA officers, and cyber/technology risk specialists

- Top candidates now need regulatory knowledge, data fluency, and communication skills alongside domain depth

- The best risk professionals aren't on job boards and require relationship-led recruiting through trusted networks to reach

What Is Risk Management in Banking?

Banking risk management is the ongoing process of identifying, assessing, and controlling threats to a bank's financial stability, operational continuity, and regulatory standing. It spans credit decisions, interest rate exposure, internal fraud, cybersecurity posture, and regulatory compliance across every business line.

That scope exists for a reason. Banks are custodians of public money — and unlike most industries, their failures don't stay internal. They operate under multilayered federal and state regulation — OCC, FDIC, CFPB, FinCEN, Basel III, BSA/AML frameworks, and more. When a bank fails, the consequences don't stay within its walls.

The 2023 failures of Silicon Valley Bank and Signature Bank made this concrete. The Federal Reserve's post-mortem on SVB found the bank had 31 open supervisory findings at the time of failure — roughly triple its peer group. It lost over $40 billion in deposits in a single day. The fallout pushed regulators, boards, and examiners to scrutinize risk governance more aggressively than at any point since 2008. For banks building out their risk functions heading into 2026, the staffing implications are direct: gaps that once drew warnings now draw enforcement.

The Core Risk Categories Banks Need to Staff For

Each of the six primary risk categories demands its own specialist knowledge. Blending them together or relying on generalists creates blind spots.

Credit Risk

Credit risk (the probability that borrowers default) is the most foundational category in banking. Credit risk professionals assess borrower creditworthiness, manage concentration risk, and set lending limits.

The standard evaluation framework — the 5 Cs — covers:

- Character: borrower's repayment history and reliability

- Capacity: income and debt-to-income ratio

- Capital: assets and reserves available

- Conditions: loan terms and economic environment

- Collateral: assets pledged to secure the loan

With credit card delinquency rates at 2.94% across commercial banks as of Q4 2025, and persistent inflation affecting borrower repayment capacity, the OCC has flagged credit risk as elevated heading into 2026.

Market Risk

Market risk covers losses from fluctuations in interest rates, FX, equity prices, and commodity values. Teams managing this function use tools like Value at Risk (VaR), stress testing, and hedging strategies — which is precisely why experienced market risk professionals remain in high demand heading into 2026.

The Federal Reserve's 2025 DFAST stress tests evaluated large bank holding companies under severely adverse scenarios, reinforcing regulatory expectations for robust quantitative risk coverage.

Operational Risk

Operational risk encompasses internal process failures, employee errors, fraud, system outages, and external disruptions. It now overlaps significantly with cyber and technology risk, expanding the required skill set well beyond what this role demanded five years ago.

Liquidity Risk

Liquidity risk is the danger that a bank cannot meet short-term cash obligations. The SVB case made the social media dimension of this risk painfully clear: research published through the FDIC showed that social media activity directly accelerated the SVB bank run, with banks experiencing heavier Twitter discussion suffering larger stock losses during the run period.

Digital banking enables near-instant mass withdrawals. Liquidity professionals now need to factor in sentiment monitoring alongside traditional cash flow modeling — a requirement that simply didn't exist a decade ago.

Compliance and Regulatory Risk

Compliance risk is exposure to fines, sanctions, and reputational damage from failing to meet regulatory obligations — AML/BSA, KYC, GDPR, CRA, capital adequacy rules. FinCEN reported 4.7 million Suspicious Activity Reports filed in FY 2024, averaging 12,870 filings per day. That volume reflects ongoing structural demand for AML analysts, BSA officers, and financial crimes investigators.

Cyber and Technology Risk

Cyber risk has become a board-level concern. The financial services sector recorded 739 data compromises in 2025 — the highest of any industry for the second consecutive year. NYDFS Part 500's final cybersecurity requirements took effect November 1, 2025, adding governance mandates around multi-factor authentication, asset inventories, and risk assessments for Class A companies.

Professionals in this space need to bridge technical vulnerabilities and regulatory frameworks. Few candidates hold both hands-on security credentials (CISSP, CISM) and working knowledge of NYDFS Part 500 or OCC guidance — which is why cyber risk hiring timelines consistently run longer than any other risk category.

Why Hiring Risk Talent Is Harder Than Ever in 2026

The Demand-Supply Gap Is Structural

The BLS projects financial examiner employment to grow 19% from 2024 to 2034 — much faster than average — but from a base of only 65,100 jobs generating roughly 5,700 annual openings. That's not a pipeline capable of meeting demand. Wolters Kluwer's April 2026 analysis puts the digital skills gap in U.S. banking at a projected 350,000 workers — and notes this cannot be closed through recruiting alone.

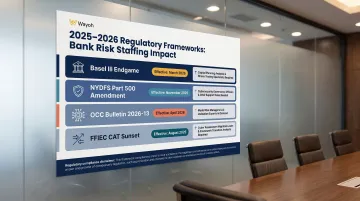

Regulatory Expansion Is Rewriting Role Scopes

New frameworks are raising the bar on existing roles, not just creating new ones:

| Framework | Effective Date | Staffing Impact |

|---|---|---|

| Basel III Endgame (revised) | Proposed March 2026 | Capital planning, RWA modeling, stress testing |

| NYDFS Part 500 Amendment | November 1, 2025 | Cybersecurity governance, MFA, asset inventories |

| OCC Bulletin 2026-13 (revised MRM guidance) | April 17, 2026 | Model risk framework redesign; AI guidance pending |

| FFIEC CAT Sunset | August 31, 2025 | Migration to alternative cyber assessment frameworks |

Take the Basel III Endgame proposal: it would increase CET1 capital requirements by approximately 16% for large banking organizations, demanding expanded teams in capital planning, risk-weighted asset modeling, and stress testing. A mid-level analyst who was qualified two years ago may not meet today's requirements.

Fintech and Non-Bank Competition

Banks no longer just compete with each other for risk talent. Fintechs, crypto firms, and insurtechs are recruiting from the same pool — often offering equity compensation, remote flexibility, and faster career progression that traditional bank structures struggle to match.

The AI Fluency Gap

As banks deploy AI-driven fraud detection, credit scoring models, and automated regulatory reporting, risk professionals need to govern and challenge these systems — not just use them. OCC Bulletin 2026-13 explicitly excludes generative and agentic AI from current model risk guidance, signaling a second wave of requirements is coming. Banks that delay hiring AI-fluent risk professionals will face a widening gap when that guidance arrives.

What AI fluency looks like in practice:

- Evaluating model inputs, outputs, and failure modes

- Documenting AI governance decisions for regulatory review

- Flagging model drift in credit scoring or fraud detection systems

- Challenging vendor-built AI against internal risk thresholds

Key Risk Roles Banks Are Prioritizing in 2026

Chief Risk Officer and Deputy CRO

The CRO role has fundamentally changed. Oliver Wyman's 2025 RMA survey of 177 CROs found the position has been transformed by the 2023 regional bank crisis, with regulators and examiners becoming considerably more demanding. The EY/IIF Global Bank Risk Management Survey — now in its 15th year — traces the evolution from compliance-centric to strategy-focused, identifying agility across diversifying risks as a top 2026 priority.

Today's CRO needs cross-domain fluency: credit, cyber, AI governance, ESG, and operational resilience — not just one or two of these. That combination is rare, which makes board-level risk leadership among the hardest searches to execute.

Finding CRO-caliber talent requires deep networks inside regulated financial institutions. Wayoh's relationship-led recruiting model (built across a decade of financial services placements in banking, fintech, and related sectors) provides access to candidates who aren't visible through job boards or standard search approaches.

Model Risk and Quantitative Analysts

Model risk management has grown substantially as banks rely on AI, ML, and statistical models for credit decisions, fraud detection, and stress testing. The April 2026 guidance (OCC Bulletin 2026-13) replaced the foundational SR 11-7 framework, applying primarily to banks with over $30 billion in assets — model risk teams at large institutions need to retrain on the new framework now.

Validators in this space need statistical expertise, regulatory knowledge, and the ability to challenge model assumptions with rigor. That intersection of quantitative skill and regulatory fluency defines a genuinely thin candidate pool.

AML/BSA Compliance Officers

SAR filing volumes have increased 9.3% in two years — from 4.3 million in FY 2022 to 4.7 million in FY 2024. That sustained growth directly translates to ongoing demand for BSA officers, AML analysts, and transaction monitoring specialists. Candidates with prior experience at regulatory agencies (FinCEN, OCC, FDIC) command higher compensation premiums — and are typically off the market within weeks.

AML, KYC, sanctions, and financial crime searches require a pre-built candidate network. Passive candidates in this discipline rarely respond to cold outreach; they move through trusted relationships.

Cyber and Technology Risk Specialists

The blending of IT and risk has created strong demand for professionals who understand both technical vulnerabilities — cloud risk, third-party vendor risk, ransomware exposure — and frameworks like NYDFS Part 500 and FFIEC cybersecurity guidance. What makes this search difficult is the narrow overlap: pure security engineers rarely have the governance fluency, while compliance-focused candidates often lack technical depth. The right hire sits at both intersections.

Operational Risk Managers

Post-pandemic, operational resilience planning has become a regulatory requirement. The Basel Committee's Principles for Operational Resilience (BCBS d516) and the OCC's Three Lines of Defense framework both require dedicated staffing across all three lines. Banks are currently hiring across multiple operational risk functions at once:

- Control framework design and documentation

- Third-party and vendor risk management

- Business continuity and recovery planning

- Regulatory reporting and examination support

How to Build a Winning Risk Hiring Strategy

Define the Role Before Sourcing

Generic job descriptions extend time-to-hire and attract unqualified applicants. Effective risk hiring starts with a specific brief covering what you actually need:

- Strategic risk leadership (CRO, VP Risk) — cross-functional, board-interfacing, regulatory relationship management

- Technical specialists (model risk validators, quant analysts) — statistical depth, regulatory knowledge, model challenge capability

- Compliance practitioners (AML officers, BSA analysts) — transaction monitoring, SAR filing, regulatory exam readiness

Role clarity at the outset keeps sourcing focused and prevents wasted cycles on candidates who are technically qualified but wrong for the scope.

Look Beyond Active Candidates

The best risk professionals in banking are typically not searching. They're employed, performing well, and not refreshing job boards. Reaching them requires trusted professional relationships — the kind built over years of conversations in a specific market, not database queries.

That dynamic is only intensifying. The BLS projects 19% growth for financial examiners against a base of 65,100 jobs — a supply-demand gap that makes passive sourcing not optional, but the primary channel for accessing top-tier risk talent.

Partner with a Specialized Financial Services Recruiter

Generalist staffing firms can source resumes, but they typically lack the regulatory vocabulary to evaluate whether a candidate actually understands DFAST methodology, SR 11-7 model risk guidance, or NYDFS Part 500 governance requirements. That gap shows up in interview quality, shortlist relevance, and ultimately in hiring outcomes.

Wayoh's focus on compliance, risk, and legal hiring — spanning over a decade and 500+ placements across regulated sectors — means faster access to candidates who are already vetted for both technical depth and regulatory fit. The network-first model reaches passive candidates through direct relationships across key U.S. markets, including New York, California, Florida, and Texas.

For banks needing interim coverage during regulatory remediation, a product launch, or an unexpected vacancy, Wayoh supports contract placements with transparent conversion options available from the start.

Frequently Asked Questions

What is banking risk management?

Banking risk management is the systematic process of identifying, assessing, and mitigating threats to a bank's financial stability and regulatory standing. It covers credit, market, operational, liquidity, compliance, and cyber risks — and requires qualified specialists at every level of the organization.

What are the primary risk categories for banks?

The six core categories are credit risk, market risk, operational risk, liquidity risk, compliance/regulatory risk, and cyber/technology risk. Each requires distinct expertise — no single professional or team can adequately cover all six without specialization.

What are the types of risk management in banking?

The traditional disciplines — credit, market, operational, liquidity, and compliance — remain the foundation. Technology adoption and AI regulatory requirements have since pushed cyber risk management and model risk management into distinct functions, each with its own hiring and oversight demands.

What are the 5 stages of risk management?

The five stages are: risk identification, risk assessment, risk mitigation, ongoing monitoring, and governance/reporting. Each stage requires qualified personnel — gaps in any one of them can surface quickly during regulatory examination.

What is governance, risk and compliance (GRC) in banking?

GRC is the integrated framework banks use to align risk management with regulatory obligations and internal governance. It follows the Three Lines of Defense model: business units own risk, risk and compliance functions provide oversight, and internal audit delivers independent assurance.

What is the role of technology in financial risk management?

AI-powered fraud detection, automated regulatory reporting, and model risk platforms have changed how banks identify and respond to risk. These tools also create new hiring requirements — banks need professionals who can govern these systems, challenge their outputs, and keep pace with evolving model risk guidance.