According to PwC's 2025 Global Compliance Survey, 85% of executives report compliance requirements have grown more complex over the past three years. Meanwhile, global regulatory fines hit a record $19.3 billion in 2024, with U.S. bank-specific penalties surging 522% year-over-year. The cost of inadequate compliance leadership is no longer theoretical.

For banking and fintech organizations, finding the right CCO has never been harder — or more consequential. This article breaks down the four major hiring trends reshaping the market, the forces driving them, and what organizations need to do differently to compete.

TL;DR

- CCO demand is rising sharply as AML, cybersecurity, ESG, and digital asset obligations expand the compliance mandate

- RegTech, AI tools, and data analytics fluency are now baseline requirements for every serious CCO candidate

- The CCO is increasingly a direct CEO or board report, signaling a structural shift from legal support to strategic leadership

- 56% of sitting CCOs are considering a move, and 51% of firms expect a compliance skills gap within 12 months

- Organizations that broaden candidate profiles and use specialized compliance recruiters will close roles faster and better

Trend 1: Tech Fluency Is Now a Baseline CCO Requirement

The Shift in What Employers Are Asking For

Five years ago, RegTech literacy appeared in CCO job descriptions as a "nice to have." Today, it's listed alongside regulatory expertise as a core qualification. Employers across banking and fintech are explicitly requiring CCO candidates to understand AI-powered transaction monitoring, automated AML screening, model risk governance, and data analytics frameworks.

The market data supports this shift. The global RegTech market is projected to reach $144 billion by 2034, growing at a 19% CAGR. That growth reflects massive institutional investment in compliance automation — investment that CCOs will be expected to oversee, evaluate, and govern.

PwC's 2025 data shows 82% of organizations plan to increase technology investment in compliance, and 71% believe AI will net-positively transform the function. The organizations planning that investment need a CCO who can direct it intelligently.

Why This Trend Won't Reverse

The volume and speed of modern regulatory obligations have outpaced manual compliance processes. Regulatory change events, transaction monitoring at scale, sanctions screening, and model-driven risk assessments cannot be managed through traditional legal training alone.

That gap has a direct hiring consequence: a CCO who excels at legal interpretation but can't evaluate an AI-driven transaction monitoring platform no longer fits the full scope of the role. Hiring briefs now consistently list these capabilities:

- Data analytics literacy and ability to interrogate compliance dashboards

- Familiarity with AML automation platforms and vendor evaluation

- Model risk governance, including understanding SR 11-7 requirements

- Oversight of AI systems used in credit decisions and fraud detection

- Evaluation of RegTech implementations and ROI

For organizations like Wayoh, which specializes in compliance leadership recruitment across banking and fintech, this shift means that candidate evaluation now includes a meaningful technology component that wasn't present in searches even three to four years ago.

Trend 2: The CCO Is Earning a True Seat at the C-Suite Table

Reporting Lines Are Changing

The traditional CCO reporting structure — through the General Counsel, with periodic board exposure — is giving way to direct CEO or board reporting. The DOJ's updated Evaluation of Corporate Compliance Programs (September 2024) specifically evaluates CCO "seniority, stature, and autonomy," and DOJ prosecutors now look for direct board or audit committee reporting lines as evidence that compliance is genuinely empowered.

The gap between aspiration and current reality remains significant. Only 38% of compliance officers are currently involved in executive strategy development, and just 40% hold C-level titles, according to a SAI360 report. For hiring teams, that gap is now a liability — regulators notice when CCO authority exists on paper but not in practice.

How This Changes the Hiring Profile

When a CCO reports to the board, the hiring criteria shift substantially. Regulatory knowledge remains essential, but it's no longer sufficient. Employers are now evaluating candidates on:

- Communicates regulatory risk clearly to non-technical audiences, including boards and investors

- Frames complex compliance exposure as governance decisions with strategic implications

- Has direct experience in M&A due diligence, new market entry, or product development — not just policy maintenance

The Banking Circle appointment of Patrick Green as CCO in May 2026 illustrates this directly — the hire was explicitly tied to the firm's digital asset expansion strategy, not just its compliance maintenance requirements. Boards want a CCO who can sit in growth conversations, not just flag what those conversations can't do.

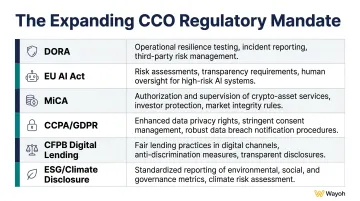

Trend 3: Expanding Mandates Are Broadening the Qualification Bar

From AML/BSA to Everything

CCO candidates in banking and fintech are now evaluated across a regulatory surface area that didn't exist a decade ago. Beyond traditional AML/BSA expertise, current CCO job descriptions routinely list:

| Regulatory Domain | Key Requirements |

|---|---|

| DORA (EU) | ICT risk management, third-party oversight, incident reporting |

| EU AI Act | High-risk AI governance in credit scoring and fraud detection |

| MiCA | Crypto-asset authorization, disclosure, digital asset AML |

| CCPA/GDPR | Consumer data privacy, cross-border data governance |

| CFPB digital lending rules | Fair lending in algorithmic underwriting environments |

| ESG/climate disclosure | Sustainability reporting, climate risk governance |

For fintech CCOs specifically, requirements increasingly include:

- Stablecoin oversight and digital asset AML

- Open banking and embedded finance governance

- BaaS compliance management

These are domains where traditional bank CCOs often have limited direct experience.

The Bifurcated Talent Market

This expansion has created two parallel CCO markets: traditional bank compliance leaders with deep AML/BSA and OCC/Fed examination experience, and fintech-native compliance leaders with crypto, digital asset, and growth-stage regulatory experience. These profiles overlap less than hiring managers often assume.

That gap directly affects the qualified candidate pool. Organizations with highly specific domain requirements will find fewer viable candidates — and the answer isn't to search for one person who covers every regulatory area. It's to hire a CCO who can architect and lead a team of specialists, rather than personally own every domain.

Trend 4: Banks and Fintechs Are Competing for the Same Scarce CCO Talent

The Compensation and Competitive Landscape

The talent competition is real and intensifying. Fintech risk and compliance hiring rose 26% year-over-year in the UK, with fintechs now accounting for over one-fifth of all risk and compliance roles — up from 12% in 2023. Meanwhile, traditional banks cut compliance hiring by 1% under cost pressure.

Compensation benchmarks reflect the pressure. According to BarkerGilmore's 2025 CCO Compensation Report, technology-sector CCOs command total compensation of up to $770,000 , a premium most banks struggle to match directly. The competitive dynamic breaks down like this:

What fintechs offer:

- Equity upside and greenfield program-building

- Speed, faster decision-making cycles, and strategic visibility

- Higher total comp at growth-stage firms

What banks counter with:

- Institutional stability and regulatory relationship depth

- Established compliance infrastructure and team support

- Prestige and long-term career credibility

Talent Scarcity Signals

The retention picture compounds the recruitment challenge:

- 56% of CCOs are considering a job search within the next year, primarily driven by compensation concerns

- 51% of firms anticipate a compliance skills gap within 12 months

- 39% of CCOs expressed concerns about job security — creating a volatile retention environment

These figures explain the rise of interim and fractional CCO arrangements. When permanent searches extend to several months — common for senior compliance leadership given role complexity and candidate scarcity — organizations need coverage. Interim CCOs bridge regulatory gaps during searches, remediation periods, and rapid-growth phases without forcing premature permanent decisions.

Why Specialized Recruiting Partnerships Matter

Both the scarcity of available candidates and the cost of a prolonged search make the sourcing model itself a critical variable. Firms that work with compliance-specialized recruiters tend to close CCO searches faster — not because of process efficiency alone, but because of direct access to candidates who aren't visible on job boards. Wayoh has placed 500+ professionals across regulated industries over more than a decade, working through direct market relationships rather than keyword-matched database searches.

The distinction matters for CCO searches specifically. Many qualified compliance leaders at the senior level aren't actively applying through job boards. They're reachable through long-built relationships in the compliance community. For organizations under regulatory pressure or mid-search without a clear front-runner, that network access often determines whether a search closes in weeks or months.

What's Driving These CCO Hiring Shifts

Regulatory Acceleration and Enforcement Costs

In 2024, U.S. AML/KYC/sanctions penalties reached $4.3 billion — 95% of the global total for these categories. TD Bank's enforcement action related to AML failures became one of the most visible institutional compliance failures of the year. When enforcement actions hit at that scale, boards take compliance leadership investment seriously.

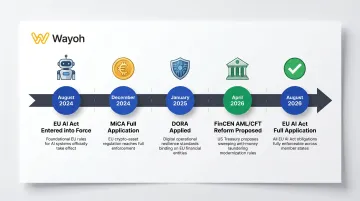

Globally, the regulatory stack has expanded dramatically. DORA applied in January 2025. MiCA fully applied in December 2024. The EU AI Act entered into force in August 2024 with full application in August 2026. FinCEN proposed fundamental AML/CFT reform in April 2026. Every addition to that stack translates directly into expanded CCO scope — and stronger hiring urgency.

Fintech Maturation and Licensing Pressure

Between January 2023 and mid-2024, federal regulators issued 124 severe enforcement actions in the BaaS space, with 64% of enforcement actions against BaaS sponsor banks involving BSA/AML deficiencies. The CFPB enforcement action against Synapse Financial Technologies for failing to maintain adequate records of customer funds illustrated what happens when fintech compliance infrastructure doesn't scale with business growth.

Early-stage fintechs that operated with lean compliance functions are now facing bank charter applications, BaaS partnership scrutiny, and IPO-readiness requirements. This creates urgent demand for first-time CCO hires — typically experienced candidates who can build programs from the ground up, not just manage established ones.

AI Governance as a Compliance Domain

The DOJ's September 2024 ECCP update now requires companies to demonstrate risk assessments for AI and emerging technologies, including whether they've established human oversight baselines for AI systems. The EU AI Act classifies AI used in credit scoring and insurance pricing as high-risk, requiring formal governance frameworks.

Federal Reserve SR 11-7 already establishes model risk management requirements for U.S. banks. CCOs are increasingly the executives responsible for ensuring these requirements are met — making AI governance literacy a baseline job requirement for the role.

Personal Liability as a Hiring Dynamic

The SEC has signaled that individual CCOs can face personal liability in cases involving misconduct or willful negligence. Direct CCO enforcement actions remain relatively rare in practice, but the directional pressure is unmistakable. Regulators at the SEC, FinCEN, OCC, and EBA are scrutinizing individual compliance leaders — not just the institutions they serve.

This raises the stakes of every CCO hire and pushes organizations to offer candidates meaningful legal protections alongside competitive pay. Typical package components now include:

- D&O coverage with adequate policy limits

- Explicit indemnification provisions in employment agreements

- Retention structures tied to regulatory milestones

Future Signals: What CCO Hiring Looks Like Next

Crypto and Digital Asset Regulation Will Create New Demand

The GENIUS Act — the first federal regulatory framework for payment stablecoins — has cleared Congress, signaling that U.S. crypto regulation is finally moving from aspiration to obligation. Add MiCA's full implementation in Europe and OCC's conditional approval of five digital asset national trust bank charters, and compliance leaders with genuine digital asset expertise will be in high demand within the next 12 to 24 months.

Fintechs operating in payments, digital wallets, and tokenized assets need CCOs who understand this landscape now — not after the regulatory frameworks mature further. Fintechs operating in payments, digital wallets, and tokenized assets need CCOs who understand this landscape now — not after the regulatory frameworks mature further. Key competencies already in demand include:

- Stablecoin reserve and redemption compliance under GENIUS Act requirements

- MiCA licensing and cross-border digital asset obligations

- OCC trust charter governance and examination readiness

AI Compliance as a Standalone Discipline

The "AI Compliance Officer" is emerging as a distinct role in financial services — separate from the broader CCO function. As AI model oversight formalizes — driven by the EU AI Act, DOJ expectations, and Federal Reserve SR 11-7 — organizations may add dedicated AI governance leads or build explicit model governance mandates into CCO job scope.

Embedded compliance functions within product teams are also emerging as a structural trend: compliance expertise placed closer to where products are built, rather than positioned solely as a review function.

These structural shifts — in both crypto regulation and AI governance — converge on a single pressure point: the talent pipeline for qualified CCOs is not keeping pace with demand.

Three-Year Outlook

- Compensation will continue rising as mandate scope expands and candidate supply tightens

- Search timelines will lengthen for organizations without proactive pipelines or specialized recruiting relationships

- Succession planning will separate organizations that sustain effective governance from those stuck in perpetual reactive search — building an internal compliance bench now is no longer optional

Organizations that move early — on recruiting partnerships, candidate criteria, and internal succession — will fill these roles. Those that don't will find themselves competing for a shrinking pool of qualified candidates at significantly higher cost.

Conclusion

Three converging forces are reshaping CCO hiring in banking and fintech: expanding regulatory complexity, a fintech sector that has outgrown its early compliance infrastructure, and technology adoption that has fundamentally changed what the role demands. The result is a position that is more valuable — and harder to fill — than ever.

Organizations that move deliberately in this environment have a clear edge. That means:

- Updating CCO hiring criteria to reflect today's regulatory and technology realities

- Broadening candidate profiles beyond traditional bank legal backgrounds

- Partnering with specialized recruiters who have built relationships with compliance leaders not actively searching

Conventional job postings reach active candidates. In a market where the most qualified CCO prospects are already employed and selectively approached, the firms that win these hires are the ones with the right networks — not just the right job descriptions.

Frequently Asked Questions

What is the role of a Chief Compliance Officer?

A CCO is the C-suite executive responsible for designing and overseeing the organization's compliance program — ensuring adherence to applicable laws, regulations, and ethical standards. In banking and fintech, this now extends to AI governance, technology oversight, and cross-functional risk management.

Is CCO a high position?

Yes. The CCO is a senior C-suite role, typically reporting directly to the CEO or board of directors, with authority over enterprise compliance and growing influence in strategic business decisions including M&A, product development, and investor communications.

What are the 5 key areas of compliance in banking?

The core domains are AML/BSA, consumer protection and fair lending, data privacy, cybersecurity compliance, and capital/prudential regulatory adherence. Fintech firms also contend with crypto asset regulation, digital lending oversight, and embedded finance governance.

What is the role of a bank compliance officer?

Bank compliance officers ensure adherence to OCC, Federal Reserve, FDIC, CFPB, and FinCEN requirements — covering AML programs, fair lending, Community Reinvestment Act obligations, consumer protection, and examination readiness. Senior CCOs translate these obligations into enterprise-wide governance programs.

What are the 7 core requirements of a compliance program?

Per the DOJ/OIG compliance framework: written policies and standards, senior leadership oversight, training and education, confidential reporting channels, internal monitoring and auditing, consistent enforcement, and prompt corrective action.

What are the 5 C's of compliance?

The five foundational pillars are Culture, Commitment, Controls, Communication, and Continuous Improvement. Effective CCOs embed these across banking and fintech compliance programs to reduce enforcement risk before regulators identify gaps.