The consequences of getting this wrong are well-documented. FinCEN assessed a record $1.3 billion penalty against TD Bank in October 2024 for allowing trillions in transactions to go unmonitored. The Federal Reserve fined Deutsche Bank $186 million in July 2023 for deficient AML controls. Both cases trace back, at least in part, to inadequate human oversight of transaction monitoring programs.

This guide is written for compliance leaders and hiring managers who need practical direction: which roles to build, what skills to require, and how to compete for qualified talent in a market where demand consistently outpaces supply.

TL;DR

- AML transaction monitoring is legally required under BSA and FATF frameworks, and technology alone doesn't satisfy that requirement

- Core roles include Transaction Monitoring Analysts, AML Investigators, BSA/AML Officers, and TMS Rules Managers, each with distinct responsibilities

- CAMS certification, TMS platform experience, and regulatory knowledge are the key differentiators when evaluating candidates

- The AML talent market is tight: 99% of financial institutions report rising compliance costs, with labor as the largest driver

- Firms that define roles precisely and work with specialized recruiters fill seats faster

What AML Transaction Monitoring Actually Requires

The Regulatory Foundation

AML transaction monitoring is the ongoing review of customer activity — deposits, withdrawals, wire transfers, account behavior — to detect patterns suggesting money laundering, terrorist financing, fraud, or sanctions evasion. For banks, fintechs, credit unions, and other regulated entities, it is a legal requirement under the Bank Secrecy Act (BSA) and FATF Recommendations.

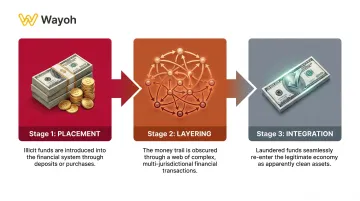

The three stages of money laundering explain why ongoing monitoring matters more than one-time onboarding checks:

- Placement — introducing illicit funds into the financial system

- Layering — disguising the trail through complex, rapid transactions

- Integration — reintroducing laundered funds into the legitimate economy

Criminals can enter and exit the financial system at any stage. Static onboarding controls only catch one entry point. Continuous transaction monitoring is what catches the rest.

Technology Doesn't Replace People

Modern TMS platforms — whether rule-based or AI-powered — automate data ingestion and flag suspicious patterns. What they cannot do is exercise judgment.

FATF's guidance on new technologies is direct on this point: "manual review and human input remains very important" and "human actors must be relied upon to identify and assess any residual risks presented by new technologies." The FFIEC goes further, requiring that automated systems be independently validated and that personnel "possess the requisite experience and investigatory tools to evaluate unusual activity."

That gap between what a system flags and what an investigator concludes is precisely where regulators focus their scrutiny. Enforcement actions consistently trace back to institutions that automated the detection but under-resourced the review — not a technology failure, but a staffing one.

Key regulatory expectations for the human layer include:

- Independent validation of automated monitoring systems

- Qualified investigators with documented experience in financial crime typologies

- Documented judgment — written rationale for alert dispositions that satisfies BSA exam standards

Key Roles on an AML Transaction Monitoring Team

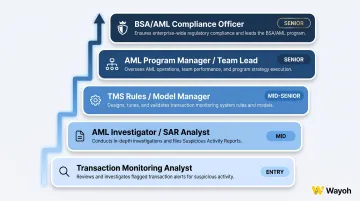

Most AML programs depend on five distinct function types — and treating them as interchangeable in hiring is where coverage breaks down.

Transaction Monitoring Analyst

The highest-volume hiring need on most teams. Analysts review system-generated alerts, conduct Level 1 investigations, and determine whether alerts are true positives or false positives requiring escalation.

This is typically an entry-to-mid-level role, but the workload is demanding. According to ACAMS, only 10% of alerts escalate to a case and just 3–5% result in a SAR filing — meaning analysts spend most of their time clearing non-productive alerts without being able to skip the review process.

AML Investigator / SAR Analyst

When an analyst flags a case for escalation, it lands with an Investigator. This role handles deeper due diligence, documents findings, and prepares Suspicious Activity Reports (SARs) for submission to FinCEN. It requires stronger regulatory knowledge and sharper investigative judgment than the analyst function — writing clear, defensible SAR narratives is a core deliverable.

BSA/AML Compliance Officer

The senior oversight role responsible for the institution's entire AML program — policy development, regulatory reporting, examiner relations, and program governance. At larger institutions, this may separate into a dedicated BSA Officer and a Chief Compliance Officer. At community banks and credit unions, one person often holds both responsibilities.

TMS Rules / Model Manager

A growing role that sits at the intersection of compliance and data analytics. Core responsibilities include:

- Configuring and tuning transaction monitoring rules

- Validating alert thresholds to reduce false positive rates

- Supporting model governance as firms move from rule-based to AI-assisted systems

As AI adoption accelerates, this hybrid function is becoming harder to fill and more strategically important.

AML Program Manager / Team Lead

Mid-to-senior management overseeing analyst teams, SLA compliance, workflow design, and coordination with technology teams. Requires both compliance depth and people management experience — a combination that narrows the candidate pool considerably.

Skills and Qualifications That Define Strong AML Hires

Regulatory Knowledge

Strong candidates at any level demonstrate working knowledge of:

- BSA — the foundational U.S. statute (31 U.S.C. 5311–5336)

- FinCEN regulations — implementing requirements and SAR filing obligations

- FATF Recommendations — international standards, especially relevant for global institutions

- OFAC sanctions — screening obligations and compliance program requirements

Senior candidates should also understand how the Anti-Money Laundering Act of 2020 and its ongoing rulemaking expansions affect program design. FinCEN published a new Notice of Proposed Rulemaking in April 2026 reforming AML/CFT program requirements. BSA Officers interviewing for senior roles should be able to speak to what those changes mean for program design.

Certifications

| Credential | Issuer | Relevance |

|---|---|---|

| CAMS (Certified Anti-Money Laundering Specialist) | ACAMS | Gold standard; required at investigator/officer level, preferred at analyst level |

| CTMA (Certified Transaction Monitoring Associate) | ACAMS | Specialized TM credential; now a differentiator for analyst and rules manager hires |

| CFE (Certified Fraud Examiner) | ACFE | Valuable for investigators, particularly in financial crime overlap cases |

TMS Platform Experience

Candidates with hands-on experience on your specific platform hit the ground faster. Prioritize familiarity with whichever system you operate. Platforms commonly referenced in financial institution deployments include:

- NICE Actimize

- Oracle Financial Services (FCCM / formerly Mantas)

- SAS Financial Crimes Analytics

- Verafin (Nasdaq)

- LexisNexis Risk Solutions

Where direct platform experience isn't available, look for candidates who demonstrate transferable proficiency — someone who has configured alert rules and tuned thresholds on one enterprise system can learn another. Requiring exact platform matches narrows an already thin candidate pool without improving hire quality.

Analytical and Investigative Skills

Beyond credentials, strong AML hires demonstrate the ability to:

- Connect disparate data points across accounts, entities, and transactions

- Recognize red flags — structuring, rapid fund movement, geographic anomalies, shell company involvement

- Write clear, factually accurate SAR narratives that would withstand regulatory scrutiny

- Maintain documentation discipline under high alert volumes

Data Literacy

Only 18% of AML professionals report having AI/ML solutions in production, per a 2025 ACAMS/SAS/KPMG survey of 850 compliance professionals. But adoption is accelerating, and the gap between firms that have deployed these systems and those still running rule-only models is widening fast.

As firms move toward hybrid AI/rule-based systems, candidates who understand how ML-driven anomaly detection works — even conceptually — carry a hiring edge. The ability to question a model's output, communicate concerns to a data science team, and explain AI-generated decisions to examiners is already shaping what compliance hiring managers are asking for in interviews.

How AI Is Reshaping AML Talent Needs

The Shift From Rules to Hybrid Systems

Traditional TMS platforms apply static rules: flag any cash deposit over $9,000 occurring twice in 10 days. Modern systems layer behavioral profiling and machine learning on top — detecting anomalies relative to a customer's established patterns rather than fixed thresholds alone.

This shift creates a new skill gap. Compliance professionals who can only work with static rule sets are less equipped to manage, validate, or explain AI-assisted outputs. Regulators expect explainability. The FFIEC requires independent validation of automated monitoring systems. Someone on your team needs to connect compliance judgment to model governance.

The "T-Shaped" AML Professional

The most effective hires for AI-assisted environments combine:

- Deep AML compliance expertise — regulatory knowledge, SAR judgment, program governance

- Adjacent technical fluency — data querying, dashboard interpretation, model governance documentation, threshold tuning logic

Traditional compliance knowledge alone leaves programs underequipped for modern TMS management. Data skills without regulatory grounding create a different problem at examination time — one that tends to surface during exams.

What This Means for Alert Review

AI reduces false positives and reprioritizes alert queues, meaning analysts handle complex, high-quality cases rather than routine threshold alerts. This raises the floor for analyst quality. Teams calibrated for high-volume, low-complexity alert clearing may find that an AI-assisted system exposes skill gaps that were previously hidden by sheer throughput.

Hiring Challenges and How to Staff Your AML Team Effectively

The Talent Shortage Is Real

The numbers tell a consistent story. Financial crime compliance cost U.S. and Canadian institutions $61 billion in 2024, with labor as the single highest cost component. 68% of AML professionals report high levels of daily work stress — a finding consistent with teams carrying more workload than their headcount supports.

Financial institutions filed 4.6 million SARs and 20.8 million Currency Transaction Reports with FinCEN in FY2023. That volume requires trained people at scale. Competition from fintechs and crypto firms — which carry their own BSA obligations — has compounded pressure on an already undersupplied talent pool.

Reactive, job-board-only hiring strategies don't work well in this environment. By the time a qualified BSA Officer or TMS Rules Manager sees a public posting, they've likely already been approached.

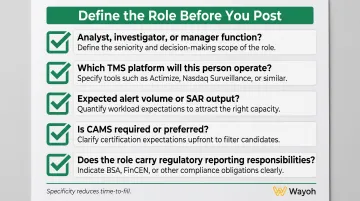

Define Roles Before Posting

Vague job descriptions attract mismatched candidates and extend time-to-fill. Before posting, answer these questions:

- Is this an analyst, investigator, or manager function?

- What TMS platform will this person operate on?

- What is the expected alert volume or SAR output?

- Is CAMS required or preferred?

- Does this role have regulatory reporting responsibilities?

Specificity filters in the right candidates and filters out mismatches before the phone screen stage.

Partner With a Specialized Recruiter to Access Passive Talent

The most experienced AML transaction monitoring professionals are rarely browsing job boards. They're identified through networks built over years in compliance recruiting.

Wayoh's approach to AML and financial crime hiring is built on this model: direct outreach, long-term market relationships, and hands-on screening rather than keyword-matched database pulls. With over 10 years in financial services staffing and 500+ placements across regulated sectors, the firm reaches both active and passive candidates — including professionals who never respond to public postings.

Wayoh supports permanent, interim, and executive search engagements across banks, fintechs, and credit unions, recruiting for roles such as:

- Transaction Monitoring Specialists

- BSA Officers

- AML Investigators

- Sanctions Analysts

- Chief Compliance Officers

For interim needs — transaction monitoring backlogs, remediation projects, KYC reviews — vetted consultants with references and background checks can move faster than permanent searches. For permanent and executive hires, a structured outreach process surfaces candidates who match both technical requirements and the regulatory environment your institution operates in.

Frequently Asked Questions

What is the transaction monitoring process in AML?

AML transaction monitoring collects customer transaction data and runs it through rule-based and/or AI-powered detection systems to flag suspicious patterns. Trained compliance analysts then investigate flagged alerts and file Suspicious Activity Reports (SARs) with FinCEN when activity warrants reporting.

How do banks do AML checks?

Banks combine KYC onboarding data, automated TMS platforms, and human analyst review. Risk-based screening ensures higher-risk customers and transaction types — such as large cash activity or international wire transfers — receive more intensive scrutiny than low-risk account behavior.

What are the five red flags in AML?

The five most common red flags are: structuring or smurfing (breaking up transactions to avoid reporting thresholds), unusually rapid fund movement, transactions inconsistent with the customer's stated business or profile, involvement of high-risk jurisdictions, and use of shell companies or layered ownership structures.

What are the three stages of money laundering?

Money laundering moves through three stages: placement (entering illicit funds into the financial system), layering (obscuring the trail through complex transactions), and integration (reintroducing laundered funds into the legitimate economy as apparently clean assets).

What are the five pillars of AML?

The five pillars are: a compliance program with internal controls, a designated BSA/AML compliance officer, ongoing employee training, independent auditing, and a risk-based customer due diligence process.

How much does AML compliance cost?

Financial crime compliance costs in the U.S. and Canada reached $61 billion in 2024, with labor as the single largest expense. Compliance officer salaries typically range from $90,000 to $132,000 per year, with BSA Officers averaging around $87,000.