Introduction

Fintech compliance management hiring has evolved from a back-office function into a strategic imperative. As fintechs scale from startup to regulated financial institution, their compliance obligations increasingly mirror those of chartered banks — and the ability to hire the right professionals is becoming a competitive differentiator, not just a regulatory checkbox.

The numbers back this up. Risk and compliance hiring in fintech rose 26% year-over-year as of late 2025, marking the sector's second consecutive year of double-digit growth. Meanwhile, regulatory penalties for global financial institutions spiked 417% in H1 2025 — a signal that enforcement is not slowing down.

Those penalty figures are reshaping hiring priorities. AML/BSA enforcement, AI governance requirements, and crypto regulations are converging simultaneously — and the talent needed to navigate all three is in short supply. This article breaks down the five trends shaping fintech compliance hiring in 2026 and what they mean for companies building these teams.

TL;DR

- Fintech compliance hiring grew 26% year-over-year — fintechs now account for over 20% of all risk and compliance roles

- Fastest-growing roles: AML/BSA Officers, RegTech-fluent analysts, and AI governance professionals

- CCOs and Compliance Directors are priority hires as bank partnerships and investor scrutiny tighten

- Talent shortages are driving up compensation and extending timelines in New York, San Francisco, and Florida

- Non-compliance costs 2.71x more than proactive investment — making talent hiring an ROI decision, not just a regulatory one

Trend 1: AML/BSA Specialist Demand Reaches Record Highs

Block Inc. (Cash App) paid $80 million to 48 state regulators in January 2025 and another $40 million to NY DFS in April 2025 — all for BSA/AML failures. FINRA fined Robinhood $26 million in March 2025 for AML deficiencies. The payments and fintech sector accounted for over $160 million in AML fines in 2025 alone.

This pattern of multi-agency, multi-jurisdiction action has moved AML compliance from a back-office function to a board-level priority.

What's Driving AML Hiring Specifically

Consent orders are now mandating compliance hires as conditions of settlement — and independent monitors are being required in the most serious cases. The expectations once reserved for chartered banks (named BSA Officers, documented AML programs, suspicious activity reporting infrastructure) now apply equally to payment platforms, lending fintechs, and neobanks.

The roles seeing the sharpest demand include:

- BSA Officers (especially with payments or crypto experience)

- AML Analysts and Transaction Monitoring Specialists

- KYC Leads and Financial Crime Investigators

- Compliance Managers with multi-state licensing experience

For fintechs in payments and digital banking, AML/BSA staffing has gone from growth-stage consideration to immediate operational necessity. Stripe is publicly recruiting a US BSA Officer for its Stripe & Bridge division, requiring 10+ years of AML/BSA leadership experience — a clear signal that even the most sophisticated fintechs are building out this function at scale.

Wayoh places AML and financial crime professionals across fintech markets including New York and Florida, working with companies from Series A through post-IPO — and demand for these roles has been consistent across all stages.

Trend 2: RegTech Fluency Becomes a Non-Negotiable Hiring Requirement

The compliance professional who cannot navigate automated transaction monitoring systems, policy management platforms, or regulatory reporting tools is increasingly screened out before the interview stage. That screening is accelerating.

The global RegTech market was valued at $11.7 billion in 2023 and is projected to reach $83.8 billion by 2033 at a 21.6% CAGR. With 98% of compliance teams now using some level of automation, platform fluency is baseline — not a differentiator.

The Skills Gap This Creates

Fintechs deploying tools like Actimize, ComplyAdvantage, or Quantexa need compliance professionals who can:

- Configure and interpret transaction monitoring logic

- Manage exception queues and escalation workflows

- Generate regulatory reports from automated systems

- Work alongside engineers when platforms need customization

Traditional compliance backgrounds — built on policy review and manual investigation — often do not include this technical fluency. The result is a structural skills gap that appears repeatedly in fintech hiring briefs.

Wayoh's experience placing compliance professionals across fintech organizations reinforces this. When fintechs request candidates for AML or financial crime roles, they're not just asking for regulatory knowledge — they want professionals who've operated inside a RegTech environment and understand how automated systems interact with compliance obligations.

74% of firms still take more than a year to implement new regulations, according to CUBE's 2025 Cost of Compliance Report. For fintechs that have deployed RegTech, that lag narrows only when the team can actually operate the tools they have. For hiring managers, that makes RegTech fluency a screening criterion, not an onboarding goal.

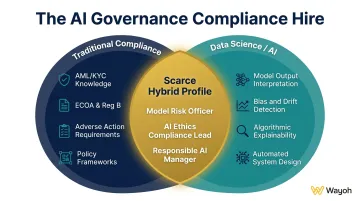

Trend 3: AI Governance and Algorithmic Compliance Roles Emerge as a New Hiring Category

Fintechs deploying AI for credit decisioning, fraud detection, and customer onboarding are creating compliance obligations that did not exist five years ago. The CFPB's Circular 2023-03 is explicit: there is no special exemption for artificial intelligence in adverse action requirements. Lenders using AI models must still provide specific, accurate reasons for credit denials under ECOA and Regulation B.

Colorado's SB 26-189, which passed the state legislature in May 2026 and is expected to take effect January 1, 2027, creates new AI governance obligations for companies using high-risk AI systems — including fintechs handling consumer financial data. At the federal level, the OCC simultaneously rescinded its 2011 model risk guidance and issued updated standards in April 2026.

What These Roles Look Like

The job titles emerging in response to these requirements include:

- Model Risk Officer — oversight of credit and fraud models for bias, drift, and explainability

- AI Ethics Compliance Lead — policy frameworks for responsible AI deployment

- Responsible AI Manager — internal governance of automated decision systems

These roles demand hybrid backgrounds. A purely traditional compliance professional lacks the data literacy to assess model outputs. A pure data scientist may not understand adverse action requirements or ECOA obligations. Candidates who can do both are scarce, and compensation reflects that — salary premiums for these hybrid profiles are visible across the market right now.

For fintech hiring teams, the regulatory exposure is already here. Any fintech using AI for consumer-facing financial decisions without qualified model risk oversight is carrying live compliance risk, not a future hypothetical.

Trend 4: Crypto and Digital Asset Compliance Specialists Enter Mainstream Demand

Digital asset compliance is no longer a niche function for crypto-native companies. Payment platforms supporting stablecoin transactions, digital wallets processing tokenized assets, and lending platforms interacting with blockchain infrastructure all carry compliance obligations that require specialized knowledge.

The FATF Travel Rule — which requires information sharing between Virtual Asset Service Providers during transfers — expanded from 65 implementing jurisdictions in 2024 to 85 jurisdictions in 2025, a 31% increase. Treasury has proposed bringing stablecoin issuers into the BSA framework. The Digital Asset Market Clarity Act (H.R. 3633) is advancing in Congress to formalize digital asset regulatory categories.

The Roles Fintechs Are Hiring

- VASP compliance specialists with FATF Travel Rule experience

- BSA/AML professionals with blockchain analytics tool experience (Chainalysis, Elliptic, TRM Labs)

- Regulatory counsel for state money transmitter licensing

- Sanctions compliance specialists familiar with OFAC's digital asset enforcement posture

Fintechs that don't self-identify as crypto companies are still getting pulled into scope. Processing stablecoin payments or touching tokenized assets triggers compliance requirements that standard AML programs often weren't built to handle.

Wayoh places compliance professionals for fintech organizations operating in this space, sourcing candidates with experience in AML and KYC controls, blockchain risk frameworks, and digital asset regulatory structures. Most in-demand candidates bring fluency across more than one background — traditional bank BSA, securities compliance, or crypto-native organizations.

Trend 5: Fintechs Shift from Outsourcing to Building Permanent In-House Compliance Teams

Early-stage fintechs historically covered compliance through fractional CCOs, outside counsel, or consultant arrangements. Regulatory and commercial pressure is forcing that model out.

What's Forcing the Shift

Two developments are accelerating this transition:

- FDIC consent orders (February 2024) required 4-year lookbacks on Customer Identification Programs and 2-year lookbacks on SAR filings from BaaS-partner banks — scrutiny that extended directly to their fintech partners. The message: if you want banking infrastructure, your compliance function needs clear, named ownership.

- OCC Bulletin 2023-17 established interagency third-party risk management standards requiring banking organizations to assess compliance infrastructure in fintech partners. A consultant arrangement doesn't meet that standard.

The result: permanent compliance hires are now prerequisites for bank-fintech partnerships, not optional infrastructure upgrades. Fintechs in the process of signing sponsor bank agreements or renewing existing relationships are engaging recruiters for full-time CCO and Compliance Director searches specifically because their banking partners are asking for them.

Wayoh supports this shift directly, running permanent Compliance Director and CCO searches for fintech teams moving from founder-led compliance to structured, accountable leadership.

What's Driving Fintech Compliance Hiring Trends in 2026

These trends don't operate independently — they're being pushed by the same set of converging pressures.

Regulatory Enforcement Escalation

The 417% spike in regulatory penalties in H1 2025 was not an anomaly. Block's $120 million across 49 regulators in four months, Robinhood's $26 million FINRA fine, and the CFPB's cumulative $19.7 billion in consumer relief enforcement since its inception — these reflect coordinated, multi-agency enforcement that is redefining what "minimum viable compliance" means for fintechs.

The Cost Math

Thomson Reuters data puts the average annual cost of compliance at $5.47 million and the average cost of non-compliance at $14.82 million — roughly 2.71 times more expensive. Compliance hiring is a financial risk management decision with a clear ROI.

Technology Creates New Roles, Not Fewer

The assumption that RegTech automation reduces compliance headcount is not holding. With 98% of firms adopting some level of automation, the demand for professionals who can govern, configure, and interpret automated systems is growing alongside the technology itself. AI governance roles are emerging as a net-new category, not a replacement for existing functions.

Talent Competition Between Banks and Fintechs

Traditional banks and fintechs now compete for the same compliance professionals. NYC's talent market has bifurcated: traditional banking operations are shedding headcount under Basel III pressures, while RegTech and AI risk roles are, in the words of one market analysis, "unable to hire fast enough at any price."

Compensation benchmarks are rising for senior fintech compliance roles, and time-to-hire for specialized positions is extending. Wayoh places compliance, risk, and legal professionals across New York, San Francisco, and Florida — and the difficulty of filling these roles quickly has become one of the most consistent challenges its fintech clients face.

How These Trends Are Reshaping Fintech Compliance Teams

The cumulative effect of these trends is changing not just who fintechs are hiring, but how compliance teams are structured and positioned within the business.

Compliance by Design Is Changing Who Gets Hired

Compliance is being embedded earlier in the product lifecycle. "Compliance by design" requires professionals who can work cross-functionally with engineering, product, and legal teams — reviewing product requirements before launch, not flagging problems afterward.

Fintechs are also mirroring bank-style three-lines-of-defense models, requiring hires across first-line operational controls, second-line compliance oversight, and third-line internal audit. Wayoh's placement process evaluates compliance candidates on cross-functional collaboration capability alongside technical regulatory knowledge — because in 2026, functional expertise alone isn't enough.

In-House Compliance Teams Now Signal Investor Credibility

A credentialed, in-house compliance team now functions as a signal of trustworthiness to institutional investors, banking partners, and regulators. Compliance hiring is tied directly to deal-making outcomes — bank partnership approvals, Series B due diligence, and licensing applications all benefit from a named, accountable compliance function.

The compliance professional profile is also changing. Fintech compliance roles in 2026 demand:

- Core regulatory knowledge (AML, KYC, BSA, UDAP, ECOA)

- RegTech platform fluency

- Data literacy for AI governance and model risk

- Cross-functional communication with product and engineering

Traditional compliance training rarely covers all four. That gap is widening the search beyond conventional candidates.

Geography still shapes the talent pool. New York remains the primary U.S. hub for fintech compliance talent, but remote and hybrid arrangements are expanding options for companies willing to structure roles that way.

Future Signals for Compliance Hiring in Fintech

Five regulatory and structural developments will drive compliance hiring demand well beyond 2026. Each one creates a distinct gap that fintech and banking firms will need to fill:

- Colorado's SB 26-189 takes effect January 1, 2027, and additional state-level AI laws are advancing across multiple legislatures — compliance teams will need dedicated oversight for automated decision systems.

- Treasury's proposed rule extending Bank Secrecy Act requirements to stablecoin issuers will force payment fintechs without an MSB history to build AML/BSA programs from scratch.

- CFPB Section 1033 data-sharing obligations phase in through 2030, creating steady demand for privacy and data governance hires as smaller institutions hit their deadlines.

- FinCEN's Investment Adviser AML Rule (now effective January 2028) means compliance buildouts for investment-adjacent fintechs are approaching, not receding.

- As AI tools automate transaction monitoring and policy review, demand will shift toward compliance engineers who can govern those systems — not just operate manual processes.

For fintech firms, acting early on these signals matters. The compliance talent market tightens as deadlines converge, and teams that begin hiring before mandates take effect consistently outpace those that wait.

Conclusion

Fintech compliance hiring in 2026 is being shaped by enforcement intensity, technological disruption, and market maturation happening at the same time. The five trends covered here — AML/BSA demand, RegTech fluency requirements, AI governance roles, digital asset compliance, and the shift to permanent in-house teams — represent both immediate hiring priorities and the longer-term trajectory for how fintech compliance functions will be built.

Fintechs that invest in compliance talent ahead of pressure will be better positioned to scale responsibly — and avoid the enforcement actions that have cost peers hundreds of millions of dollars. That means:

- Hiring AML specialists before regulators flag gaps

- Building RegTech-fluent teams before a bank partnership is at stake

- Securing senior compliance leadership before investor due diligence surfaces problems

Getting that hiring right — especially at speed — is where a specialized recruiter makes the difference. Wayoh has over a decade of experience placing compliance, risk, and legal professionals across major U.S. fintech markets, with 500+ placements across regulated industries. Whether a company needs its first compliance hire or is building out a full three-lines-of-defense structure, Wayoh's network-first approach and deep regulatory market knowledge can compress time-to-hire without sacrificing candidate quality.

Frequently Asked Questions

What is compliance in fintech?

Fintech compliance refers to a financial technology company's adherence to laws, regulations, and industry standards governing financial services — including AML, KYC, data privacy, consumer protection, and licensing requirements. It covers both federal obligations (BSA, ECOA, CFPB rules) and state-level requirements that vary by jurisdiction.

What is the role of compliance in fintech?

Compliance in fintech protects consumers, prevents financial crimes, and enables the company to operate legally across jurisdictions. A strong compliance function also signals operational maturity to institutional investors, banking partners, and regulators.

What are the 4 phases of compliance?

Most compliance frameworks follow four phases:

- Identification — understanding which regulations apply to the business

- Assessment — evaluating current gaps against those requirements

- Implementation — building the controls, policies, and procedures to close gaps

- Monitoring — ongoing review and updating as regulations and business activities evolve

What compliance roles are most in demand at fintech companies in 2026?

AML/BSA Officers, RegTech Compliance Analysts, Chief Compliance Officers, AI Governance and Model Risk professionals, and Digital Asset Compliance Specialists are among the most actively recruited roles. Senior compliance leadership is particularly sought after as fintechs mature and banking partnerships require accountable in-house ownership.

What skills do fintech compliance professionals need in 2026?

Beyond core regulatory knowledge (AML, KYC, UDAP, BSA), fintechs now expect familiarity with RegTech platforms, data analysis, AI risk frameworks, and cross-functional collaboration with product and engineering teams. Tech fluency is no longer optional — it's a baseline requirement.

How does fintech compliance hiring differ from traditional bank compliance hiring?

Fintech compliance hiring prioritizes tech fluency and the ability to build programs from scratch, not just maintain inherited frameworks. Fintechs move faster than traditional banks, so candidates must be comfortable operating in environments where policy gaps and new product launches occur at the same time.