For early-stage fintechs, the response isn't always to hire a full-time CCO immediately. The fractional model — experienced, senior compliance leadership engaged on a part-time or retainer basis — has become the practical middle ground for companies that need real compliance ownership without the full-time overhead.

This guide walks through what a fractional CCO actually does in a fintech context, when the model makes sense, how costs compare, what qualifications to prioritize, and how to run the hiring process effectively.

TLDR

- A fractional CCO provides senior compliance leadership on a retainer or project basis, serving as an ongoing program owner rather than a one-off advisor

- Common triggers include pursuing licensing, entering bank partnerships, preparing for a regulatory exam, or scaling an AML/KYC program

- Full-time CCO total compensation runs $180K–$380K+ at Series A through C; fractional engagements typically range $10K–$30K/month

- The right candidate brings fintech-specific experience: AML program builds, MTL applications, and direct regulator interactions — not just broad financial services credentials

What Is a Fractional Chief Compliance Officer — and What Do They Do in Fintech?

A fractional CCO is an experienced compliance executive who works on a part-time, retainer, or project basis. Unlike a consultant brought in for a one-time deliverable, a fractional CCO maintains ongoing accountability for the compliance program — they know your regulatory relationships, your risk profile, and your business model.

"Fractional" describes the engagement structure, not the commitment level. The compliance obligations are the same; what changes is how the executive's time is allocated across the business.

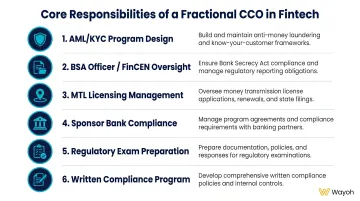

Fintech-Specific Responsibilities

In a fintech context, a fractional CCO typically owns:

- Designing and overseeing AML/KYC programs — transaction monitoring, customer due diligence, and enhanced due diligence frameworks

- Serving as BSA Officer under FinCEN's requirements for MSBs, including SAR and CTR filing oversight

- Managing money transmitter license applications across states, including AML documentation and state banking department coordination

- Satisfying sponsor bank audit rights and the compliance infrastructure requirements banks enforce before and during BaaS relationships

- Handling regulatory correspondence, information requests, and FFIEC-aligned exam preparation

- Drafting and maintaining the written compliance program, marketing review policies, and internal controls documentation

This is C-suite work. A fractional CCO advises founders, represents the company in front of regulators, and shapes compliance culture from the inside out.

Because fractional CCOs work across multiple clients at once, they also bring something an in-house hire rarely develops as quickly: pattern recognition. They see what regulators are scrutinizing across different company types — and that cross-client exposure often surfaces risks before they become exam findings.

When Should a Fintech Hire a Fractional CCO?

The fractional model isn't only for companies that can't afford a full-time hire. It's often the strategically correct structure when compliance workload is event-driven or scaling rather than consistently high and predictable.

Four Trigger Scenarios

1. Approaching a licensing application or bank partnership States like Florida and Oklahoma require a functional AML program at the time of MTL application, not after approval. A full 50-state MTL rollout takes 18–24 months. Fintechs entering sponsor bank relationships face similar requirements: under the June 2023 Interagency Guidance on Third-Party Relationships, banks must verify that fintech partners meet BSA/AML standards before and throughout the partnership.

Compliance leadership must be in place before applications begin.

2. First regulatory examination or inquiry When an exam notice arrives, there's no time for a 3–5 month hiring process. A fractional CCO sourced through a specialized network can be operational within days. Wayoh supports fintech companies specifically at these inflection points — audit preparation, exam readiness, and urgent compliance leadership gaps — drawing on a network built across more than a decade of regulated-industry placements.

3. Launching a regulated product or entering new states Adding a lending product, a payments feature, or expanding into new states creates distinct licensing obligations and compliance requirements. These are contained, high-stakes workstreams that fit the fractional model well.

4. Existing team is under-resourced for a new regulatory demand If your internal compliance team handles routine operations competently but a new CFPB rulemaking or evolving SAR reporting standard requires depth beyond their current capacity, a fractional CCO can run the new workstream without displacing the baseline program.

Not every company stays on the fractional model indefinitely. When compliance risk is consistently high and regulatory relationships require daily management, a full-time hire makes more sense. At that stage, continuous C-suite presence in board meetings and investor conversations becomes necessary — and the fractional model introduces availability risk that a permanent hire eliminates.

Fractional CCO vs. Full-Time CCO: Cost and Fit

The Cost Comparison

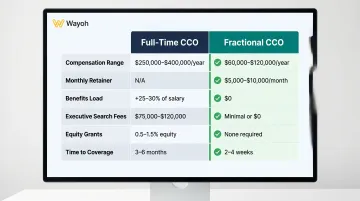

| Factor | Full-Time CCO | Fractional CCO |

|---|---|---|

| Base + bonus (Series A) | $180,000–$230,000 | N/A |

| Base + bonus (Series B–C) | $250,000–$380,000 | N/A |

| Monthly retainer | N/A | $10,000–$30,000/month |

| Benefits load (20–30%) | $36,000–$114,000 | Not applicable |

| Executive search fees (20–30% of comp) | $50,000–$114,000 | Reduced or none |

| Equity grants | Common at early stage | Rarely required |

| Time to productive coverage | 3–5 months | Days |

Fractional engagements can deliver 30–50% cost savings versus maintaining a full in-house compliance function, according to industry benchmarks. At the low end of fractional rates ($10K/month), annual cost is $120K — well below the total cost of ownership for a full-time Series A hire once benefits, search fees, and equity are factored in.

Non-Cost Factors That Matter

Beyond dollars, three operational advantages favor the fractional model for early-stage fintechs:

- Deploys in days, not months — a meaningful difference when a licensing event or regulatory exam is already on the calendar

- Scales with your compliance calendar — hours increase during exam periods or MTL application sprints, then return to steady-state

- Carries no equity dilution or severance exposure — a relevant constraint for seed and Series A companies managing their cap table

When Full-Time Wins

The fractional model has clear limits. If your compliance calendar is consistently full, if regulators expect a named CCO who is reachable daily, or if board and investor conversations require standing C-suite presence, a fractional arrangement introduces availability and continuity risk that full-time headcount resolves.

That said, fractional engagements tend to make the eventual full-time search faster and better-defined. Documented compliance programs, established regulatory precedent, and a scoped job description arrive pre-built — the permanent hire steps into structure rather than starting from scratch.

What Qualifications Should You Look For?

General financial services compliance experience is not sufficient for a fintech CCO role. The regulatory environment is specific, and vetting should reflect that.

Must-Have Experience Markers

- Built or overhauled AML/KYC programs for payment companies or MSBs — not just oversight, but hands-on program construction

- Holds BSA Officer designation with demonstrated SAR/CTR filing history and direct regulator-facing accountability

- Managed money transmitter licensing across multiple states — multi-state MTL experience is materially different from single-state

- Navigated bank-fintech partnership compliance, including sponsor bank audits and negotiating compliance representations in partnership agreements

- Conducted direct regulator interactions with FinCEN, CFPB, OCC, or state banking departments — regulator familiarity is not the same as regulatory experience

Credentials Worth Verifying

- CAMS (Certified Anti-Money Laundering Specialist, ACAMS) — the primary AML credential, held by 65,000+ professionals globally; relevant for all fintech compliance leadership roles

- CRCM (Certified Regulatory Compliance Manager, ABA) — requires 3–6+ years of U.S. banking compliance experience; relevant for bank partnership and federal regulatory work

- For crypto or digital asset contexts, ACAMS also offers the CAFCA (Certified AML FinTech Compliance Associate) and CCAS (Certified Cryptoasset Anti-Financial Crime Specialist) designations

How to Assess Communication Fit

A fractional CCO needs to do more than know the rules. They'll advise founders who have no compliance background, convert regulatory requirements into product constraints that engineering teams can actually act on, and hold up under scrutiny in regulator conversations. A technically qualified candidate who can't communicate those constraints clearly can stall a product launch or create gaps that surface during an exam.

Wayoh's evaluation process for compliance leadership roles explicitly assesses founder compatibility, communication style, and how candidates perform under pressure alongside credentials and regulatory exposure.

How to Run the Hiring Process for a Fractional CCO

Step 1: Scope the Engagement Before Sourcing

Vague scopes attract generalists. Before approaching candidates or recruiters, define:

- The regulatory environment the role must cover (MSB, bank partner, lending product, crypto)

- Hours per month expected under steady-state versus peak conditions

- First 90-day deliverables (AML program gap assessment, MTL application, exam prep)

- Engagement structure: ongoing retainer versus defined project with optional extension

Step 2: Vet Through Compliance-Specific Criteria

Credentials matter, but references tell you more. Ask candidates directly:

- Which regulatory examinations have you managed, and what was the outcome?

- Have you built an AML program from scratch? What did the initial gap assessment reveal?

- Which MTL states have you navigated, and what compliance documentation did you prepare?

- Describe a FinCEN or CFPB inquiry you responded to — what was your approach?

Reference checks with prior fintech clients are more informative than reviewing credentials alone.

Step 3: Use a Specialized Recruiting Channel

The qualified candidate pool for fintech fractional CCO roles is narrow. CAMS requires 18–24 months of specialized experience minimum; CRCM requires 3–6+ years of U.S. banking compliance work. Most candidates with the right profile are passive — they're not actively browsing LinkedIn or general job boards.

Wayoh's compliance recruiting practice works through direct outreach and long-term market relationships rather than keyword searches. With 500+ placements across regulated industries — including fintech companies from Seed to Series C — that model matters most when the timeline is short and the cost of a wrong hire is high.

Frequently Asked Questions

What is a fractional chief compliance officer?

A fractional CCO is an experienced compliance executive engaged on a part-time or retainer basis to provide senior-level program leadership — covering AML/KYC oversight, regulatory relationships, BSA Officer responsibilities, and policy design. The engagement is ongoing, not a one-time project, and the CCO maintains continuous accountability for the compliance function within their agreed scope.

How much does a fractional chief compliance officer cost?

Fractional CCO engagements typically run $10,000 to $30,000 per month depending on scope, complexity, and experience level, with hourly rates around $200–$400/hour. Annual retainer cost starts at roughly $120K — well below the $180K–$380K+ total compensation of a full-time CCO hire at Series A through C.

When should a fintech hire a fractional CCO instead of a full-time one?

The fractional model fits best when compliance workload is event-driven — licensing applications, first regulatory exams, new product launches, or bank partnership launches. When compliance risk is consistently high, regulatory relationship volume requires daily management, or the company needs standing C-suite presence, a full-time hire is the better structure.

What is the difference between a fractional CCO and a compliance consultant?

A consultant delivers a defined project — a gap assessment, a policy review, a training session — then exits. A fractional CCO takes ongoing ownership of the compliance program, serves as BSA Officer, and maintains regulatory relationships as a part-time executive. The output is a functioning, continuously managed program, not a deliverable document.

How long does it take to onboard a fractional CCO?

Fractional engagements sourced through a specialized recruiter or established professional network can be operational within days. Full-time CCO searches take 3–5 months on average from job posting through notice period and onboarding — a timeline that creates real legal exposure during a licensing event or exam notice.