Banking, fintech, and healthtech face a higher bar than most industries because every hire carries downstream regulatory consequences. And "compliant hiring" in these sectors means two distinct things: following employment law while recruiting, and hiring people who carry the right credentials, registrations, and regulatory history to do their jobs legally. Most hiring guides address the first. This article addresses both.

TLDR: Key Takeaways

- Regulated industries have compliance rules that govern both the hiring process and which candidates are eligible for specific roles

- Compliance gaps rarely surface in real time — they appear during audits, regulatory reviews, or when a credentialed hire turns out not to be

- Most hiring failures trace back to late-stage role checks, inconsistent documentation, or over-reliance on a single compliance resource

- A specialized recruiting partner reduces both the risk of hiring non-compliant candidates and running a non-compliant process

What Makes Hiring in Regulated Industries Different

Most industries require employers to follow employment law when hiring. Regulated industries require that and something harder: every new hire's credentials, licenses, and regulatory history can directly affect the firm's own compliance standing.

A BSA officer with undisclosed sanctions history isn't just a bad hire — they're a regulatory liability. A healthtech firm that onboards a privacy officer without proper credential verification doesn't just have an HR problem; it creates immediate HIPAA exposure.

The Regulators Who Shape Who You Can Hire

The bodies that govern these sectors don't just set rules for what your organization does. They set expectations for who can hold certain roles within it:

Banking & fintech regulators:

- FINRA — registration and qualification requirements

- OCC — BSA/AML competency standards

- FinCEN — AML program enforcement

- CFPB — FCRA compliance in background screening

Healthtech regulators:

- HHS/OCR — HIPAA privacy officer requirements

- HHS OIG — exclusion screening via the LEIE

- FDA — QMSR personnel qualification documentation for SaMD firms

Meeting those standards requires the right people. That's where regulated hiring gets harder.

The Talent Shortage Accelerates the Risk

Demand for qualified compliance professionals consistently outpaces supply — and when teams are under pressure to fill seats, speed is where compliance breaks down.

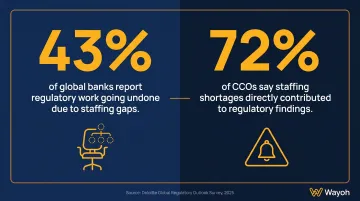

According to a 2025 Deloitte survey, 43% of global banks report regulatory work going undone due to staffing gaps. That same research found 72% of CCOs say staffing shortages directly contributed to regulatory findings.

The pressure to fill critical roles fast doesn't suspend regulatory requirements — it just increases the odds of getting them wrong.

Temporary Placements Carry the Same Requirements

One of the most common assumptions that creates compliance exposure: that contract or interim hires don't require the same verification rigor as permanent employees. They do.

FINRA Rule 1210 requires registration of all persons engaged in a member's securities business — regardless of employment arrangement. Temporary compliance officers, interim BSA leaders, and contract risk analysts placed into regulated environments must meet the same credential and background standards as permanent hires. Generalist staffing firms typically overlook this entirely.

Unique Compliance Hiring Challenges in Banking, Fintech, and Healthtech

Each of these sectors shares a commitment to regulatory oversight. But the specific hiring compliance requirements differ meaningfully. What a bank needs to verify before placing a BSA officer is not the same as what a healthtech firm needs before onboarding a HIPAA privacy officer.

Banking

FINRA-registered roles require verification before a hire is made — not after. Under FINRA Rule 3110(e), firms must verify the accuracy and completeness of all information in an applicant's Form U4. This includes criminal and civil records, judgments, liens, bankruptcies, and business affiliations. Delays don't just slow the process; they can trigger FINRA violations.

CRA officers, BSA/AML officers, and Fair Lending analysts carry defined competency standards under OCC and FinCEN guidance. The FFIEC BSA/AML Examination Manual directs examiners to assess whether the BSA compliance officer demonstrates actual knowledge of BSA regulations, not just a title.

Background check timing is particularly sensitive. Adverse credit history or prior regulatory sanctions are disqualifying for certain banking roles. Running these checks late wastes time and creates legal exposure around the two-step adverse action notice process required under FCRA.

Fintech

Fintechs face a structural challenge: rapid growth combined with role types that didn't exist five years ago. Crypto compliance officers, AI risk analysts, and open banking specialists often lack established credential benchmarks, which makes it harder to verify that a candidate actually knows what the role demands.

The regulatory environment adds further complexity. State money transmitter licenses vary by product type, and under the CSBS Model Money Transmission Modernization Act, compliance officers at licensed money transmitters are classified as "key individuals" subject to specific requirements:

- Submit fingerprints for FBI background checks

- Disclose criminal convictions, regulatory actions, and civil litigation

- Maintain documented records of these disclosures

Earlier-stage fintechs rarely track these obligations — and the gap tends to surface at the worst possible time.

Worker classification is another overlooked exposure. Growth-stage pressure to hire contractors is understandable, but misclassifying a compliance or risk professional can raise questions from regulators about whether the firm has adequate internal oversight.

Healthtech

Healthtech firms handling protected health information (PHI) must verify HIPAA privacy officer credentials and state medical licensing for clinical roles. For SaMD firms, FDA's QMSR adds another layer: it took effect February 2, 2026, and requires documented evidence that staff affecting product quality are competent.

On healthcare background checks, the HHS OIG states that employing an excluded individual can trigger civil monetary penalties of up to $20,000 per item or service billed, plus treble damages. Screening against the LEIE isn't optional, and it needs to happen before day one.

State-level requirements add another layer. Many healthcare facility access rules require background checks to be completed before first-day access, not concurrent with onboarding. Hiring processes designed for less regulated industries routinely miss this distinction.

Where Compliant Hiring Breaks Down Most Often

Compliance Requirements Aren't Embedded in the Workflow

The most common failure mode isn't ignorance — it's informality. Credential verifications and licensing checks exist as mental reminders rather than system checkpoints. They get done when someone remembers and skipped when someone is busy — and because there's no record either way, they never get audited.

This is how a firm ends up six months post-hire realizing that a candidate's U4 history was never reviewed.

Documentation Fragmentation Is an Audit Liability

Interview feedback lives in email threads. Approvals happen in verbal conversations. Candidate documents are spread across personal folders and shared drives. In regulated industries, this isn't just disorganized — it's a direct audit risk.

If you cannot reconstruct the decision trail for a hire made six months ago, you cannot prove it was done compliantly. Auditors look for consistency and documentation. The absence of either is a finding.

Speed Pressure Creates Structural Compliance Risk

According to SHRM, speed has risen to the top of employer priorities when selecting background screening providers — switching places with accuracy. In regulated industries, that tradeoff carries real consequences.

An unfilled compliance or risk role creates its own regulatory exposure. But cutting verification steps to fill it faster creates a different, often larger one. A missed credentialing step discovered post-hire is far more costly than a slower, documented process.

The Institutional Knowledge Trap

When compliance requirements for specific roles live in the head of one senior recruiter, the entire process becomes fragile. That person goes on leave, changes roles, or isn't available — and hiring either stalls or moves forward without the right checkpoints.

This is particularly dangerous in regulated environments where role-specific requirements aren't intuitive to generalist HR professionals. The knowledge needs to be in the process, not the person.

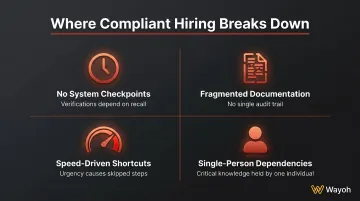

Each of these breakdowns shares a common thread: they're structural, not situational. Fixing them requires embedding compliance checkpoints directly into the hiring workflow — not relying on individual memory or informal coordination.

- No system checkpoints — verifications depend on individual recall rather than process triggers

- Fragmented documentation — no single audit trail means no defensible compliance record

- Speed-driven shortcuts — urgency pressures teams to skip or defer verification steps

- Single-person dependencies — role-specific knowledge held by one person creates critical process gaps

Key Elements of a Compliant Hiring Process for Regulated Sectors

Embed Checkpoints Directly Into the Hiring Workflow

A structurally sound compliant hiring process doesn't rely on people remembering what to check. Role-specific credential verifications and licensing confirmations are built into the workflow as required steps — not optional reminders. Screening criteria are applied consistently across all candidates for the same role. Auditors don't expect perfection — they look for consistency, and a well-structured workflow is the clearest evidence of it.

Know Which Jurisdiction Governs Each Role

That consistency becomes harder to maintain the moment hiring crosses state lines. A firm placing roles in New York, California, and Florida is operating under three meaningfully different legal environments simultaneously:

- Ban-the-box laws: As of 2025, 37 states plus D.C. have enacted restrictions on when criminal history can be considered. New York's Article 23-A and California's Fair Chance Act each require individualized assessments after a conditional offer.

- Pay transparency: New York requires salary ranges in job postings for employers with 4+ employees. California's SB 1162 applies to employers with 15+ employees. Florida has no equivalent requirement.

- Healthcare licensing compacts: The Nurse Licensure Compact (41 jurisdictions), IMLC (43 jurisdictions), and others create faster pathways to multi-state practice — but firms must verify which states participate and which credentials transfer.

Multi-state regulated firms need jurisdiction awareness built into every search from the start.

Documentation Standards That Survive an Audit

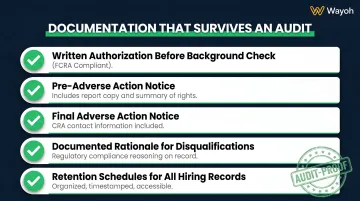

The specific documentation elements most often missing when audits surface compliance gaps:

- Written authorization before any background check (FCRA requirement)

- Pre-adverse action notice — including a copy of the report — before any adverse decision

- Final adverse action notice with CRA contact information after a reasonable waiting period

- Documented rationale when disqualifying a candidate on regulatory grounds

- Retention schedules for all hiring records

For regulated firms, each of these is a mandatory requirement — and missing even one creates documented exposure during an audit.

How a Specialized Recruiting Partner Reduces Your Compliance Risk

What Generalist Agencies Miss

A generalist staffing agency knows how to screen for skills. It generally doesn't know what a U4 filing means, when adverse credit history is disqualifying versus irrelevant, or which state licensing requirements apply to a healthtech hire in a clinical-adjacent role. For banking, fintech, and healthtech positions, that knowledge gap is a material risk — not a minor inconvenience.

What Wayoh Brings to the Table

With over a decade in financial services staffing and 500+ placements across compliance, risk, and legal roles, Wayoh's recruiters understand the regulatory landscape that governs these hires. The firm's relationship-led model means candidates are known quantities: vetted through direct conversations, reference checks, and background screening.

That translates to concrete differences at each stage of hiring:

- Candidates arrive pre-assessed against the regulatory requirements relevant to their role

- Recruiters can evaluate regulatory exposure and compliance experience beyond what a resume shows

- Deep market knowledge covers banking (FINRA, OCC, FinCEN), fintech (CFPB, state money transmitter frameworks), and healthtech (HIPAA, CMS, state licensing boards)

- For emerging fintech roles without established credential benchmarks — crypto compliance, AI risk — Wayoh assesses practical regulatory experience and domain knowledge rather than defaulting to credentials that don't yet exist

Same Rigor for Temporary and Permanent Placements

That same standard applies regardless of engagement type. Interim compliance leadership and contract placements — whether supporting an audit, a product launch, or a transition — receive the same vetting rigor as permanent searches. Wayoh conducts full reference checks and background screening before placement, with weekly engagement throughout the assignment to keep performance on track and flag issues early.

For firms that need immediate compliance leadership but aren't ready to commit to a permanent hire, Wayoh offers transparent conversion terms from day one, so organizations can convert to a permanent hire once the fit is clear.

Frequently Asked Questions

What are regulatory compliance services for regulated industries?

Regulatory compliance services help organizations meet legal and operational standards set by bodies like FINRA, OCC, CFPB, or CMS. In hiring, this covers recruitment practices, documentation, licensing verification, and candidate eligibility for specific roles.

What does it mean to work in a regulated industry?

Working in a regulated industry means operating under rules set by government agencies that define what your organization can do, who can hold certain roles, and what standards must be maintained. In banking, fintech, and healthtech, these rules affect everything from product design to personnel decisions.

What are some examples of regulated industries?

Banking, fintech, healthcare, healthtech, pharmaceuticals, insurance, and energy are among the most heavily regulated industries in the U.S. Each is overseen by specific federal and/or state bodies with authority to investigate, fine, or sanction non-compliant organizations.

What is the 70/30 rule in hiring?

The 70/30 rule suggests candidates should meet roughly 70% of stated requirements at hire, developing the remaining 30% on the job. In regulated industries, this has clear limits — certain licenses, credentials, and background standards are non-negotiable regardless of overall candidate fit.

What compliance checks are required when hiring for financial services roles?

Common requirements include FINRA licensing and U4/U5 history checks, criminal background checks, credit reviews for roles with financial authority, and certification verification (CAMS for AML, CFA for investment roles). FCRA and FINRA rules require completing these checks at defined points in the hiring process.

How does a specialized staffing agency help with compliant hiring in regulated sectors?

A specialized agency brings knowledge of licensing requirements, credential standards, and documentation practices that generalist firms lack. Candidates arrive pre-screened against the right regulatory standards, and the process is structured to hold up under audit scrutiny.