Introduction

Financial institutions now depend on dozens — sometimes hundreds — of third-party vendors for core functions: cloud infrastructure, payment processing, KYC platforms, core banking software, fraud detection. That dependency has fundamentally changed what vendor oversight means. Oversight now requires active, ongoing risk management embedded in operations — not just annual questionnaire reviews.

The problem most banks and fintechs face is a talent gap. The 2023 Interagency Guidance from the OCC, FDIC, and Federal Reserve makes clear that institutions cannot outsource responsibility for vendor failures — but finding professionals who combine financial services regulatory knowledge with genuine third-party risk expertise remains difficult. Few candidates hold both deep regulatory fluency and hands-on TPRM program experience.

What follows breaks down what VRM roles actually look like in financial services, which qualifications matter most, and where hiring teams tend to go wrong — leaving firms exposed when examiners come knocking.

TL;DR

- VRM in financial services spans cyber, compliance, operational, and legal risk — it requires dedicated specialists, not repurposed compliance generalists

- OCC, FDIC, FFIEC, and Federal Reserve frameworks place explicit accountability on institutions — regardless of vendor behavior

- Strong VRM hires combine regulatory fluency, risk methodology, and contract review skills — all three together are rare in the open market

- Vague job descriptions and job-board-only searches routinely miss the passive candidates who fill these roles best

- Specialized recruiters with financial services networks can materially reduce time-to-fill for these hard-to-source roles

What Makes Vendor Risk Management Uniquely Complex in Financial Services

Regulators Don't Accept "We Outsourced It" as an Answer

The 2023 Interagency Guidance is unambiguous: using a third party "does not diminish or remove a banking organization's responsibility to ensure activities are conducted in a safe and sound manner." That principle puts VRM squarely in the category of board-level concern, not IT procurement.

The enforcement record confirms this isn't theoretical. In 2024 alone, the Federal Reserve issued actions against Evolve Bank & Trust and First & Peoples Bank for deficiencies tied to third-party risk failures. Lineage Bank received an FDIC consent order requiring specific improvements to its third-party oversight program. And the Synapse Financial collapse revealed an $85 million gap between depositor liabilities and partner bank funds — a direct consequence of inadequate vendor oversight.

The Breadth of Risk Categories

What makes VRM genuinely difficult is that vendor failures rarely stay contained. A single vendor breach can simultaneously trigger:

- A cybersecurity incident requiring regulatory notification

- An operational downtime event affecting customer service

- A compliance finding if the vendor handled regulated data improperly

- Reputational damage requiring executive response

VRM professionals must navigate operational, cyber, compliance, credit, concentration, and reputational risk — and understand how these categories interact. That cross-domain fluency is what separates a capable VRM hire from a specialist in any single risk area.

Continuous Monitoring Has Replaced Annual Reviews

Point-in-time assessments are no longer the standard. Regulators expect evidence of ongoing monitoring, not just a due diligence questionnaire filed at onboarding. Firms need staff who can build and sustain living oversight programs. In practice, that means:

- Tracking vendor changes and ownership events

- Reviewing updated SOC 2 reports on a defined cycle

- Monitoring news and threat intelligence on critical vendors

Fourth-Party Risk Adds Another Layer

According to the Ncontracts 2026 State of TPRM Survey, 26% of financial institutions do not assess fourth-party risk at all — meaning they have no visibility into their vendors' vendors. For cloud and fintech partners specifically, subcontractor dependencies can create concentration risks that aren't visible without close analysis. Strong VRM hires understand this dimension and know how to evaluate it through contract provisions and SOC 2 subservice organization disclosures. Finding candidates who can operate at that level of technical depth — across all these risk categories — is what makes VRM hiring genuinely hard to get right.

The VRM Roles Financial Services Firms Need to Fill

LinkedIn currently lists over 5,000 vendor risk management positions in the United States, and Deloitte's 2023 Global TPRM Survey found 34% of TPRM leaders cite labor-market shortages as a significant headwind. Demand is real and sustained. Here's how the role landscape breaks down.

Third-Party Risk Analyst

The execution layer of any VRM program. Analysts typically handle:

- Conducting due diligence questionnaires

- Reviewing SOC 2 Type 2 reports

- Scoring vendors by risk tier

- Tracking ongoing monitoring activities

This role suits candidates with 2–4 years in compliance, audit, or operational risk. It requires genuine specialization — not a rotation assignment for someone between functions.

Vendor Risk Manager / Third-Party Risk Manager

This is the program owner. Responsibilities include:

- Managing the full vendor lifecycle from onboarding through offboarding

- Maintaining the vendor inventory and risk tiering framework

- Building audit-ready documentation

- Coordinating across legal, compliance, IT security, and business lines

Candidates for this role need genuine program management experience, not just familiarity with the concepts. There's a meaningful difference between someone who has executed due diligence tasks and someone who has designed and owned a program.

Vendor Compliance Officer / Third-Party Compliance Specialist

A more legally oriented role focused on regulatory alignment. This professional ensures that vendor contracts and oversight processes satisfy FFIEC guidance, OCC requirements, GLBA Safeguards Rule obligations, and applicable state requirements. Often embedded within a broader compliance function at mid-size and larger institutions.

Director or Head of Third-Party Risk

The most difficult role to fill. This position sets enterprise-wide VRM policy, owns regulator-facing documentation, reports to the CRO or board, and leads a team of analysts and managers. Candidates need genuine leadership experience alongside deep domain knowledge. That combination is rare, which is why these searches take longer and require a more targeted approach.

A note on contract and interim staffing: Given how hard Director-level talent is to source, mid-size banks and fintechs often bring in interim VRM professionals to cover the gap. For firms building programs from scratch or managing a leadership transition, interim staffing keeps program momentum and examiner readiness intact while the permanent search runs its course.

Skills and Qualifications That Define a Strong VRM Hire

The Core Competency Stack

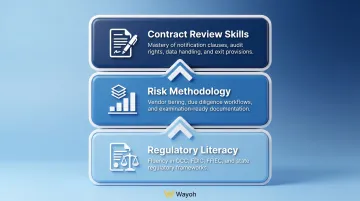

The strongest VRM candidates bring three things together:

- Regulatory literacy — understanding what OCC, FDIC, FFIEC, and state regulators actually expect from third-party oversight programs, not just what the policy document says

- Risk methodology — the ability to tier vendors by inherent risk, design proportionate due diligence frameworks, and document findings in a way that holds up under examination

- Contract review skills — identifying gaps in notification clauses, audit rights, data handling obligations, and exit provisions

Each of these matters independently. Candidates who are strong in one but weak in the others create blind spots that surface during regulatory reviews.

Technical Knowledge

At minimum, VRM professionals should be fluent in:

- SOC 2 Type 2 report interpretation (not just confirming one exists, but understanding what the controls actually cover and what exceptions mean)

- Cybersecurity assessment frameworks, particularly the FFIEC Cybersecurity Assessment Tool

- Cloud risk concepts, including shared responsibility models and data residency considerations

For senior roles, add: reviewing business continuity plans, evaluating security posture reports, and understanding fourth-party subcontractor relationships in cloud environments.

Certifications That Signal Credibility

| Certification | Issuing Body | What It Signals |

|---|---|---|

| CTPRP (Certified Third-Party Risk Professional) | Shared Assessments | Purpose-built for VRM; the most specific credential |

| CERP (Certified Enterprise Risk Professional) | American Bankers Association | Broad enterprise risk foundation in banking |

| CRCM (Certified Regulatory Compliance Manager) | American Bankers Association | Regulatory compliance depth in banking contexts |

The CTPRP is the only certification specifically dedicated to third-party risk. Candidates holding it command a compensation premium — the credential requires five years of risk management experience and a rigorous closed-book examination.

The Soft Skills That Actually Differentiate Candidates

Beyond credentials, strong VRM professionals:

- Communicate risk findings clearly to non-technical business stakeholders and board members

- Influence vendor behavior and remediation timelines without direct authority

- Maintain documentation discipline that holds up under examiner scrutiny — because they understand what gets tested

Regulatory Pressure Making VRM Talent More Critical Than Ever

The current governing framework is the 2023 Interagency Guidance (OCC Bulletin 2023-17 / FDIC FIL-29-2023), issued jointly by the OCC, FDIC, and Federal Reserve. It replaced all prior standalone agency guidance and covers the full vendor relationship lifecycle: planning, due diligence, contract negotiation, ongoing monitoring, and termination.

The guidance requires risk management practices "commensurate with the level of risk, complexity, and size of the banking organization" — meaning examiners expect qualified internal personnel, not just policy documents. That phrase, "necessary expertise and resources," translates directly into staffing expectations.

Examiners don't just review written policies. They look for:

- Consistent monitoring activity with documented evidence

- Completed vendor reviews tied to identified responsible staff

- Personnel who can speak to vendor relationships during examination

A firm with thorough policy documentation but no dedicated VRM personnel will still receive findings.

For fintechs operating under bank sponsor relationships or pursuing charters, a mature VRM function with dedicated staffing is increasingly a prerequisite. Regulators and partner banks evaluate whether the firm can demonstrate operational VRM maturity, not just written intent.

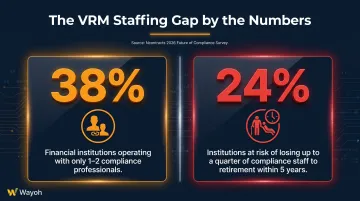

That operational maturity is hard to sustain without adequate headcount. The Ncontracts 2026 Future of Compliance Survey found 38% of financial institutions operate with only one or two compliance professionals, and 24% could lose up to a quarter of their compliance staff to retirement within five years. Firms with thin VRM staffing aren't just understaffed — they're one examiner visit away from a significant finding.

Common Hiring Mistakes When Building a VRM Team

Treating VRM as a Lateral Move for Junior Compliance Staff

This is the most common error firms make. A compliance analyst with two years of regulatory monitoring experience can document processes — but that's where the overlap with VRM ends. The skills that actually matter in a VRM role look different:

- Designing a risk tiering framework for a diverse vendor population

- Evaluating a SOC 2 report for meaningful control gaps, not just completeness

- Leading vendor remediation conversations when issues surface

VRM requires specific third-party risk experience, not just compliance familiarity. Firms that skip this distinction end up with programs that pass a documentation review but fall apart under operational scrutiny.

Writing Generic Job Descriptions

Many financial institutions write VRM postings by borrowing language from operational risk or IT security job descriptions. The result is a posting that doesn't accurately describe the role, attracts mismatched candidates, and extends time-to-hire.

Effective VRM job descriptions distinguish between:

- Program-building scope (strategic, senior)

- Program-operating scope (mid-level, execution-focused)

- Due diligence support scope (junior, analyst-level)

Each level requires a different candidate profile, sourcing strategy, and interview process. Conflating them in a single posting makes it harder to attract the right person at any level.

Sourcing Only Through Job Boards

The most experienced VRM professionals in financial services are rarely active job seekers. They're embedded in existing programs, often passive candidates who won't apply to a generic posting but will respond to a direct, informed outreach from someone who understands their background. Relying solely on job boards largely misses this pool.

How to Find and Hire Qualified Vendor Risk Professionals

Start with Role Clarity

Before sourcing begins, define what the role actually needs to accomplish:

- Program builder: Senior and strategic; right for institutions standing up a VRM function or overhauling an existing one

- Program operator: Mid-level and execution-focused; right where the framework exists but needs consistent management

- Due diligence analyst: Junior support; right where higher-level program management is already in place

Each profile requires a different sourcing approach, different compensation expectations, and different interview criteria. Mixing them up early creates problems throughout the hiring process.

Work with Recruiters Who Understand the Regulatory Context

The most effective path to qualified VRM talent in financial services runs through recruiters who know the domain — not just the job titles. A recruiter who can evaluate whether a candidate's "third-party risk experience" was substantive program ownership or peripheral compliance support is doing fundamentally different work than one keyword-matching resumes.

For senior VRM roles in particular, the candidate pool is small and the wrong hire carries real regulatory exposure. Wayoh addresses this by combining 10+ years of compliance and risk placements across banking and fintech with a network built on direct relationships rather than automated matching. That combination surfaces qualified active and passive candidates faster than open-market sourcing typically allows.

Consider Whether Permanent or Interim Staffing Fits the Moment

Once you've identified the right recruiter, the next question is hiring structure. Not every VRM need requires a permanent hire. Firms in the following situations often benefit from interim or contract VRM professionals:

- Standing up a new third-party risk program

- Covering a departure while a permanent search runs

- Addressing a regulatory finding that requires immediate program remediation

- Supporting a fintech preparing for a bank partnership review

Wayoh supports both permanent and interim placements, with vetted candidates and structured engagement throughout each assignment.

Frequently Asked Questions

What is vendor risk management?

Vendor risk management is the process of identifying, evaluating, monitoring, and governing the risks that third-party vendors introduce to an organization. It covers operational, cyber, compliance, and reputational risk across the full vendor lifecycle — from onboarding through offboarding.

What is financial services risk management?

Financial services risk management refers to the structured identification and mitigation of risks — credit, market, liquidity, operational, compliance, and third-party — that regulated financial institutions face. Oversight responsibilities are defined by regulators including the OCC, FDIC, Federal Reserve, and FFIEC.

What are the 5 C's of risk management?

The most widely recognized "5 C's" in financial services are the 5 C's of Credit: Character, Capacity, Capital, Collateral, and Conditions — used to evaluate borrower creditworthiness. There is no single standardized 5 C's framework for general risk management, though some institutions develop their own variations internally.

What roles are responsible for vendor risk management at a bank or fintech?

VRM responsibilities typically sit with a Third-Party Risk Manager or Vendor Risk Manager, overseen by a Director of Third-Party Risk or Chief Risk Officer. Compliance and legal teams are closely involved in contract review and regulatory alignment.

What certifications are most valuable for vendor risk management professionals?

The CTPRP (Certified Third-Party Risk Professional) from Shared Assessments is the most specific credential for VRM roles. The CERP (Certified Enterprise Risk Professional) and CRCM (Certified Regulatory Compliance Manager), both from the American Bankers Association, provide recognized banking-specific risk and compliance foundations.

How long does it typically take to hire a vendor risk manager in financial services?

Open-market hiring for experienced VRM professionals typically exceeds standard time-to-fill benchmarks due to the specialized skill set required and limited active candidate pool. Working with a specialized recruiter who maintains vetted relationships with passive candidates in compliance and risk functions can meaningfully reduce time-to-fill — Wayoh, for example, draws on 500+ placements across compliance and risk functions to surface qualified candidates faster than open-market searches alone.