That gap is more common than most institutions acknowledge. Banks routinely invest in risk technology and governance documentation while underinvesting in the specialized talent that makes those systems function. The result: frameworks that look complete on paper but underperform under regulatory scrutiny.

This blog covers what enterprise risk management actually means for banks, how the COSO framework structures it, which risk categories demand dedicated expertise, and what it takes to staff a team capable of delivering on the ERM mandate.

TL;DR

- ERM is a bank-wide, top-down process for identifying and managing financial, operational, compliance, strategic, and reputational risks in coordination with a bank's strategic objectives.

- The COSO 2017 framework — built around five components including Governance, Strategy, and Performance — forms the structural backbone of modern bank ERM.

- Banks face nine OCC-defined risk categories, each requiring specific monitoring approaches and specialist expertise.

- A high-impact ERM team requires clearly defined roles across all three lines of defense, from CRO to internal auditors.

- Demand for qualified ERM professionals consistently outpaces supply, making hiring gaps one of the most underestimated obstacles to effective ERM programs.

What Is Enterprise Risk Management for Banks?

Enterprise risk management is a top-down, institution-wide process that enables banks to identify, assess, and respond to risks across financial, operational, compliance, and strategic dimensions simultaneously, rather than managing each in a separate silo.

The OCC Comptroller's Handbook defines ERM as a framework that helps the board and management "view the bank's risks in a comprehensive and integrated manner," enabling identification of risk concentrations that "may arise across multiple business lines which, when aggregated, require board attention and management action."

ERM vs. Traditional Risk Management

The critical distinction is integration. Traditional risk management (TRM) isolates risks by function — credit, compliance, and operational teams each managing their own silos. ERM replaces that with a unified view tied to the bank's strategic objectives and risk appetite.

| Dimension | Traditional Risk Management | Enterprise Risk Management |

|---|---|---|

| Scope | Function-specific | Institution-wide |

| Risk view | Siloed by category | Integrated and aggregated |

| Strategic alignment | Limited | Central to framework |

| Board visibility | Selective reporting | Comprehensive oversight |

| Risk appetite | Often implied | Formally defined and monitored |

Why ERM Is Non-Negotiable in Banking

Bank failures ripple well beyond individual institutions — into depositors, credit markets, and the broader economy. That systemic exposure is why regulators mandate structured ERM across asset tiers:

- Dodd-Frank Section 165 requires bank holding companies with $50B+ in assets to establish board-level risk committees and appoint a Chief Risk Officer

- Basel III (transition period began July 1, 2025; full compliance by July 1, 2028) standardizes capital requirements and enhances risk data aggregation requirements

- SR 16-11 requires institutions under $100B to maintain board-approved risk appetite and enterprise-wide risk identification and control

- BSA/AML obligations generated approximately 4.8 million Suspicious Activity Reports and 21.5 million Currency Transaction Reports in fiscal year 2024 alone, per FinCEN

Core Components of a Bank's ERM Framework

Most U.S. banks structure their ERM programs around the COSO 2017 framework, which organizes risk management into five interrelated components with 20 underlying principles. The framework is notable for explicitly integrating risk with strategy and performance — not treating it as a separate compliance function.

Governance and Culture

The board and senior leadership establish risk oversight responsibilities, define risk appetite, and set the tone for how risk is treated across the institution. This isn't an HR initiative. Risk culture is either set at the top or it doesn't take hold. Regulators assess it accordingly.

The OCC's heightened standards require the Chief Risk Executive to have unfettered access to the board and to remain independent of the business lines that generate risk. Board involvement in the CRO's selection and compensation is a regulatory requirement, not a best practice suggestion.

Strategy, Objective-Setting, and Performance

Risks can't be meaningfully identified until strategic objectives are established. This component connects risk appetite to planning — every significant objective carries an inherent risk profile that must be assessed at the transaction, portfolio, and enterprise levels.

Risk assessments cover both inherent risk (before controls) and residual risk (after controls are applied). The gap between the two is where control effectiveness is measured.

Risk Response and Control Activities

Banks have four response options for every identified risk:

- Accept — acknowledge the risk and absorb potential losses

- Avoid — exit the activity generating the risk

- Reduce — implement controls to lower likelihood or impact

- Transfer — shift the risk to a third party (insurance, hedging)

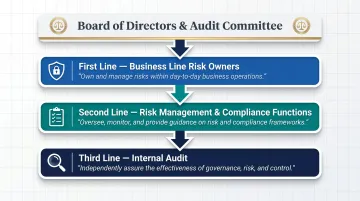

Control activities — policies, procedures, dual controls — operationalize the chosen response. The Three Lines of Defense model provides the governance structure: business lines own risk (first line), risk and compliance functions provide independent oversight (second line), and internal audit provides independent assurance to the board (third line).

Review, Revision, and Reporting

Ongoing monitoring, stress testing, and risk audits allow banks to track positions against established limits and validate that controls are actually working. Transparent reporting to regulators is mandatory. That reporting obligation carries real infrastructure implications.

The Basel III Endgame's BCBS 239 principles require globally systemically important banks to maintain capabilities for timely risk data aggregation — a direct driver of technology investment in this component for larger institutions. Key capabilities this demands include:

- Accurate, consolidated risk data across business lines

- Automated aggregation that supports same-day reporting under stress

- Clear data lineage and governance to satisfy examiner scrutiny

Key Risk Categories Every Bank ERM Team Must Address

The OCC defines nine recognized risk categories for bank supervision:

- Credit, interest rate, liquidity, and price risk

- Foreign exchange and transaction (operational) risk

- Compliance, strategic, and reputation risk

These categories are not mutually exclusive — any product or service can expose a bank to multiple risks simultaneously.

Three categories consistently generate the highest operational demands on ERM teams:

Compliance Risk

Compliance costs in U.S. and Canadian financial institutions reached $61 billion in 2023, according to LexisNexis Risk Solutions. Smaller institutions (under $10B in assets) saw a 78% rise in labor-related compliance costs. BSA/AML, CFPB enforcement, and evolving regulations require dedicated specialist expertise — this category cannot be managed by generalists.

Cybersecurity Risk

Classified under operational/transaction risk by the OCC, cybersecurity has grown into a standalone staffing priority. The IBM Cost of a Data Breach 2024 report found the average breach cost in financial services reached $6.08 million — 22% above the global average. Financial firms took an average of 168 days to identify a breach and 51 days to contain it.

Operational Risk

Process failures, IT system vulnerabilities, and third-party relationships all fall here. The 2023 interagency guidance (OCC Bulletin 2023-17) requires banks to apply structured risk management across the full life cycle of all third-party relationships, including fintech partnerships, creating significant monitoring obligations at every stage.

Emerging Categories: ESG and Model Risk

Beyond the established OCC categories, ESG and model risk now warrant dedicated functions at mid-to-large banks, driven by mounting regulatory pressure:

- The Federal Reserve conducted a pilot climate scenario analysis with the six largest U.S. banks in 2023, though OCC withdrew its climate guidance in March 2025 — the regulatory trajectory remains in flux

- Interagency model risk management guidance is expected to supersede SR 11-7, with attention focused on institutions over $30 billion in assets and expanded oversight of AI and model governance — verify current regulatory status before citing in formal documentation

How to Build a High-Impact Bank Risk Team

ERM frameworks don't execute themselves. The quality of the team running them is the primary determinant of whether the program delivers real protection or just documentation. Treating it as an org chart exercise rather than a talent architecture problem is how gaps form.

The Three Lines as a Staffing Blueprint

The Three Lines model maps directly to hiring requirements, with distinct skill profiles at each level:

First Line (Business Line Risk Owners)

- Own and manage risk day-to-day within their functions

- Need risk awareness embedded in operational decision-making

- Not dedicated risk professionals, but require risk training and accountability

Second Line (Risk Management and Compliance Functions)

- Independent of the business lines they oversee

- Includes the CRO, Enterprise Risk Managers, Compliance Officers, and Risk Analysts

- Regulatory independence is both a structural safeguard and a formal requirement

Third Line (Internal Audit)

- Provides independent assurance to the board on the effectiveness of governance, risk management, and internal controls

- Must be structurally independent — reporting to the audit committee, not management

Core Roles in a Bank's ERM Function

| Role | Primary Focus | Reporting Line |

|---|---|---|

| Chief Risk Officer | Strategic oversight, board-level reporting, framework ownership | Board/Risk Committee |

| Enterprise Risk Manager / VP of Risk | Framework execution, risk assessments, KRI tracking | CRO |

| Compliance Officers | BSA/AML, CFPB, regulatory monitoring | CRO or CCO |

| Risk Analysts | Quantitative modeling, stress testing, data analysis | ERM / VP of Risk |

| Internal Audit Professionals | Independent control evaluation, audit program management | Audit Committee |

Role clarity and reporting independence for second- and third-line roles are regulatory expectations, not organizational preferences. Conflicts of interest in risk oversight are a finding risk in themselves.

Banks that need to build or restructure these functions quickly often work with specialized financial services recruiters. Wayoh focuses on compliance, risk, and control function hiring across community, commercial, regional, and investment banks. The firm sources both permanent and interim candidates across all three lines, with placements spanning over a decade of financial services recruiting.

Essential Skills and Credentials for ERM Professionals

Technical Competencies

The growing complexity of risk data has raised the baseline for technical capability across all ERM roles:

- Quantitative risk modeling — stress testing, scenario analysis, expected loss calculations

- Regulatory knowledge — Basel III/COSO frameworks, BSA/AML requirements, SR 16-11 expectations

- Data analytics — KRI tracking, dashboard development, risk reporting automation

- Technology risk — third-party risk management, AI model governance, cyber risk frameworks

Key Credentials

In competitive hiring markets, certifications have shifted from differentiators to baseline expectations:

- FRM (Financial Risk Manager) — GARP-issued; per the 2024 GARP Risk Careers Survey, over 40% of respondents said FRM is listed as preferred or required in job postings

- CRCM (Certified Regulatory Compliance Manager) — ABA-issued; requires minimum 3 years of U.S. compliance experience; standard expectation for BSA/AML and compliance-heavy roles

- CIA (Certified Internal Auditor) — IIA-issued; held by more than 220,000 professionals across 170 countries; the recognized standard for internal audit functions

- RIMS-CRMP (Certified Risk Management Professional) — experience-based ERM generalist credential from RIMS

Soft Skills That Actually Differentiate

Technical qualifications get a candidate screened in. These are what separate strong performers from technically qualified hires:

- Communicating risk findings to non-technical stakeholders, including the board

- Cross-functional collaboration with business lines, technology, and legal teams

- Sound judgment under uncertainty — risk decisions rarely come with complete information

This combination — technical depth, regulatory fluency, and the ability to influence decisions at the executive level — is what banks are now treating as the standard profile for mid-to-senior ERM hires, not an exceptional one.

Challenges in Staffing and Scaling ERM Functions

Demand for qualified ERM professionals consistently outpaces supply. The Bureau of Labor Statistics projects 19% growth for financial examiners through 2034 — classified as "much faster than average" — with approximately 5,700 annual job openings. Compliance officers represent a workforce of 418,000 with steady replacement-driven demand.

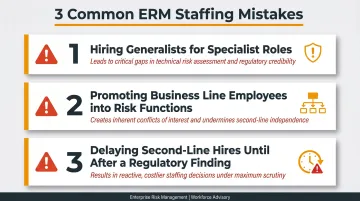

Three Common Staffing Mistakes

Banks building ERM functions make predictable errors:

- Hiring generalists for specialist roles — BSA/AML compliance and model risk are not interchangeable skill sets; staffing them with broad risk professionals creates coverage gaps that surface under examination

- Promoting business line employees into risk functions — high performers in revenue roles often lack the independence mindset and technical foundation that second-line roles require

- Delaying second-line hires until after a regulatory finding — reactive hiring under consent order conditions is more expensive, more rushed, and more likely to produce poor fit

Where Specialist Recruiting Adds Value

These mistakes share a common root: the best candidates for senior and specialist risk roles are typically not actively job hunting. Reaching them requires established professional relationships — not job postings.

Wayoh's recruiting model is built around that reality. The engagement process covers:

- Role scoping and talent market mapping

- Passive candidate outreach through direct professional networks

- Candidate vetting, interview management, and onboarding support

- Interim placements for urgent needs — audit preparation, regulatory remediation, leadership transitions — held to the same vetting standards as permanent hires

For banks facing time pressure — a regulatory finding, rapid expansion, or a key departure — that means access to pre-vetted candidates with relevant institutional backgrounds, without the lag of a cold search.

Frequently Asked Questions

What is enterprise risk management for a bank?

ERM is a bank-wide, top-down process for identifying and managing all categories of risk — financial, operational, compliance, strategic, and reputational — in alignment with the institution's risk appetite and strategic goals. It replaces function-specific, siloed risk management with an integrated view that requires board-level oversight.

What is the enterprise risk management framework for banks?

An ERM framework is the structured set of components that guides how a bank designs, implements, monitors, and improves its risk management practices. Most U.S. banks align to the COSO 2017 model, organized around five components spanning governance through reporting.

What are the 4 pillars of enterprise risk management?

The four operational pillars most commonly cited are risk identification, risk assessment, risk response, and risk monitoring. These represent how banks detect, measure, address, and track risks throughout the organization.

What are the 5 components of enterprise risk management?

Per the COSO 2017 framework: Governance and Culture, Strategy and Objective-Setting, Performance, Review and Revision, and Information, Communication, and Reporting. This is the structure most U.S. banks use to organize their ERM programs.

How much does enterprise risk management cost for banks?

Costs vary significantly by size and complexity. Deloitte reports compliance operating costs have risen over 60% compared to pre-crisis levels, while LexisNexis pegged total financial crime compliance costs at $61 billion across U.S. and Canadian institutions in 2023. Key cost drivers include personnel, GRC technology, audit functions, and regulatory training.

What are the 7 components of enterprise risk management?

The original COSO 2004 framework defined eight components — covering areas from internal environment and objective setting through risk response, control activities, and monitoring. The current COSO 2017 framework consolidates these into five components, which is the version most banks align to today.