Introduction

Cryptocurrency has entered the financial mainstream, and with it, regulatory enforcement against money laundering has intensified dramatically. In 2025, illicit cryptocurrency transactions reached a record $154 billion, driven by a 694% surge in sanctions evasion. Meanwhile, enforcement penalties have reached unprecedented levels: Binance paid $4.3 billion in 2023, OKX paid $504.7 million in 2025, and Binance's CEO Changpeng Zhao was sentenced to four months in prison for compliance failures.

This guide is for compliance leads, founders, and operators at crypto and fintech companies who need a clear, practical understanding of what AML compliance requires — and the consequences of getting it wrong. Whether you're building your first AML program or stress-testing an existing one, here's what you need to know.

TLDR:

- AML compliance for crypto firms includes KYC, transaction monitoring, Travel Rule implementation, and SAR filing

- Illicit crypto transactions hit a record $154 billion in 2025; single enforcement actions now exceed $4 billion

- FATF, FinCEN, EU MiCA, and the GENIUS Act set overlapping but distinct obligations across jurisdictions

- Blockchain transparency is both a risk (pseudonymity, cross-border speed) and a compliance advantage (permanent transaction history)

- Building an AML program requires technology, experienced financial crime professionals, and written policies from day one

What Is AML Compliance and Why It Matters in Crypto

Defining AML Compliance

Anti-Money Laundering (AML) refers to the body of laws, regulations, and internal procedures designed to prevent criminals from disguising illegally obtained funds as legitimate income. Money laundering typically occurs through three stages:

- Placement - Entering illicit funds into the financial system

- Layering - Obscuring the source through complex transactions

- Integration - Reintroducing cleaned funds as legitimate assets

In the crypto context, AML refers specifically to the compliance obligations that Virtual Asset Service Providers (VASPs) must implement. VASPs include:

- Cryptocurrency exchanges

- Wallet providers

- Lending platforms

- Payment processors

- Stablecoin issuers

Each of these entities must implement internal controls, customer verification, and transaction monitoring to prevent digital assets from being used to launder money or finance terrorism.

Why AML Compliance Is Non-Negotiable for Crypto Fintechs

The compliance obligations above aren't theoretical — regulators are enforcing them with escalating force. These recent cases show what's at stake:

| Company | Fine Amount | Date | Core Failures |

|---|---|---|---|

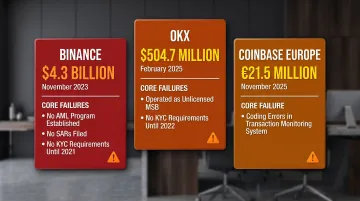

| Binance | $4.3 billion | November 2023 | No AML program; never filed a SAR; no KYC until Aug 2021; facilitated $898M+ in US-Iran trades |

| OKX | $504.7 million | February 2025 | Unlicensed MSB; no KYC until late 2022; $1T+ in US transactions without proper controls |

| Coinbase Europe | EUR 21.5 million (~$25M) | November 2025 | Transaction monitoring coding errors affecting 30M+ transactions (EUR 176B) |

Regulators no longer distinguish between intentional violations and technical failures. Coinbase's coding error resulted in a multi-million euro penalty — no bad intent required.

Beyond fines, AML failures carry operational and reputational consequences:

- Loss of customer trust and platform credibility

- Frozen institutional partnerships and banking relationships

- Sustained regulatory scrutiny requiring independent compliance monitors

- License revocations threatening business continuity

- Binance CEO Changpeng Zhao served four months in federal prison — a precedent that put every crypto executive on notice about personal liability

For crypto fintechs at any stage, the question is no longer whether AML compliance matters — it's whether your program can withstand the level of scrutiny regulators are now applying.

Why Cryptocurrencies Create Elevated Money Laundering Risk

The Financial Action Task Force (FATF) identified three primary risk factors that make cryptocurrencies particularly susceptible to money laundering:

1. Anonymity and Pseudonymity

Crypto wallets don't require identity verification at the protocol level. While blockchain transactions are recorded publicly, they're linked to wallet addresses, not real-world identities. This allows transactions with limited traceability unless an intermediary (like an exchange) captures KYC data.

2. Cross-Border Reach

Crypto moves globally without jurisdiction checkpoints. Illicit funds can be transferred instantly across borders, complicating surveillance and enforcement. FATF notes: "VAs can be used to quickly move funds globally, nearly instantaneously and largely irreversibly."

3. Lack of Centralized Oversight

Unlike traditional banking, where financial institutions monitor accounts and flag suspicious activity, crypto transactions can occur peer-to-peer without any VASP involvement. This disintermediation eliminates the compliance checkpoints that exist in traditional finance.

How Money Laundering Occurs in Crypto

Criminals exploit these characteristics through three stages:

Placement:

- Converting illicit fiat to crypto via exchanges or ATMs

- Using peer-to-peer platforms that lack KYC requirements

- Purchasing crypto through unregulated offshore exchanges

Layering:

- Moving funds through multiple wallets to obscure trails

- Using mixers and tumblers to blend funds from multiple users

- Chain-hopping between blockchains (Bitcoin → Monero → Ethereum)

- Structuring transactions below reporting thresholds (smurfing)

Integration:

- Cashing out through exchanges with weak compliance

- Converting crypto into real assets (real estate, luxury goods)

- Using NFT purchases and sales at inflated prices

Tools Criminals Use to Evade Detection

FATF's Red Flag Indicators report identifies specific evasion tactics:

- Crypto mixers and tumblers — Break transaction chains by pooling funds from multiple wallets, making source tracing extremely difficult

- Privacy coins — Monero and Zcash use cryptographic techniques that hide sender, receiver, and transaction amounts by design

- DeFi protocols — Permissionless exchanges execute swaps without identity checks, leaving no KYC trail

- Unregulated exchanges — Offshore platforms in jurisdictions with weak AML enforcement accept deposits with minimal scrutiny

The Compliance Counterpoint: Blockchain Transparency

Despite these risks, public blockchains maintain a permanent, immutable transaction history. Blockchain analytics tools — Chainalysis, Elliptic, TRM Labs — allow compliance teams to trace fund flows across wallets and flag suspicious activity with a precision that's genuinely impossible with traditional cash laundering.

Cash leaves no digital footprint once it changes hands. On-chain activity does. That asymmetry is why well-resourced AML programs treat blockchain analytics as a core investigative capability, not an optional add-on.

Core AML Requirements for Crypto Fintechs

Know Your Customer (KYC) and Customer Due Diligence (CDD)

KYC is the first line of AML defense. VASPs must verify customer identity through:

- Government-issued ID

- Proof of address

- Source-of-funds documentation

For high-risk customers—including Politically Exposed Persons (PEPs) or users in high-risk jurisdictions—Enhanced Due Diligence (EDD) applies, requiring deeper verification and more frequent review.

CDD doesn't end at onboarding. Firms must assign risk ratings to customers and update those ratings as account behavior evolves — material changes in transaction patterns should trigger re-assessment.

Transaction Monitoring and Suspicious Activity Reporting

Transaction monitoring involves systematically reviewing platform activity for patterns indicating potential money laundering:

- Transactions structured just below reporting thresholds

- Sudden spikes in account activity

- Rapid movement of funds across multiple wallets

- Transfers to or from high-risk jurisdictions

When suspicious patterns are detected, VASPs must file Suspicious Activity Reports (SARs) with FinCEN or the applicable regulator.

Unlike traditional banking, crypto gives compliance teams a unique advantage: the ability to trace on-chain transaction histories, assess wallet provenance, and enrich internal monitoring with on-chain intelligence. This makes it possible to detect illicit fund flows that cross multiple intermediaries.

The Travel Rule

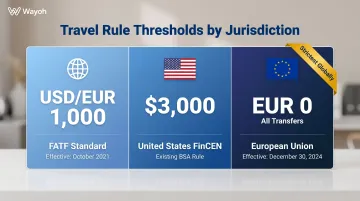

The FATF Travel Rule requires VASPs to collect, verify, and transmit originator and beneficiary information alongside virtual asset transfers above a jurisdiction-set threshold. This mirrors wire transfer transparency requirements in traditional finance.

Travel Rule compliance requires technical infrastructure for data sharing between VASPs — particularly complex for cross-border transfers involving counterparties in jurisdictions with varying thresholds:

| Jurisdiction | Threshold | Effective Date |

|---|---|---|

| FATF standard | USD/EUR 1,000 | October 2021 |

| United States (FinCEN) | $3,000 | Existing BSA rule |

| EU (Regulation 2023/1113) | EUR 0 (all transfers) | December 30, 2024 |

The EU's zero-threshold approach is the strictest globally, requiring originator/beneficiary data transmission on every CASP-involved transaction.

AML Program Documentation and Staff Training

A compliant AML program must include:

- Written policies and procedures

- A designated Money Laundering Reporting Officer (MLRO) responsible for oversight and regulatory reporting

- Regular employee training so all staff can identify suspicious activity

- Clear escalation protocols so staff know exactly when and how to report concerns

The US and Global Regulatory Landscape for Crypto AML

United States

Most US crypto firms are classified as Money Services Businesses (MSBs) under FinCEN and must register and comply with the Bank Secrecy Act (BSA). Key obligations include:

- Registering with FinCEN within 180 days

- Maintaining a written AML program

- Filing Suspicious Activity Reports (SARs)

- Filing Currency Transaction Reports (CTRs)

GENIUS Act (2025): Signed into law on July 18, 2025, the GENIUS Act brought payment stablecoins under BSA obligations for the first time. Stablecoin issuers must now maintain full AML and sanctions compliance programs, including:

- 100% reserve backing with liquid assets

- Monthly public disclosures of reserve composition

- Technical capability to seize, freeze, or burn stablecoins when legally required

OFAC Sanctions Screening: The Office of Foreign Assets Control (OFAC) published dedicated guidance for the virtual currency industry in October 2021. Key requirements include:

- Screening against the SDN List (which includes known virtual currency addresses)

- Reporting blocked virtual currency to OFAC within 10 business days

- Implementing five essential compliance components: management commitment, risk assessment, internal controls, testing/auditing, and training

State-Level Complexity: New York's BitLicense (23 NYCRR Part 200) adds compliance obligations beyond the federal baseline, including minimum capitalization requirements ($500,000 surety bond) and transaction monitoring standards.

Global Standards and Frameworks

FATF (International Baseline): The FATF Updated Guidance (October 2021) sets the international standard. It requires countries to:

- Assess and mitigate VA-related money laundering and terrorist financing risks

- License or register VASPs

- Apply AML/CFT requirements equivalent to those for financial institutions

- Implement the Travel Rule

EU MiCA Regulation: Markets in Crypto-Assets (MiCA) entered into force in June 2023, establishing a comprehensive authorization and supervisory framework for Crypto-Asset Service Providers (CASPs) across EU member states. The companion Transfer of Funds Regulation (EU 2023/1113) applies the zero-threshold Travel Rule from December 30, 2024.

UK FCA: Crypto firms must register with the FCA under the Money Laundering Regulations 2017 (MLRs). The FCA plans a new "FCA Gateway" for broader cryptoasset regulated activities, with applications opening September 30, 2026.

Crypto's cross-border nature means fintechs operating internationally must map obligations across multiple frameworks simultaneously. Where jurisdictions diverge, VASPs must apply the strictest applicable standard per transaction, determined by the originator and beneficiary locations.

Red Flags: Signs of Money Laundering in Crypto Transactions

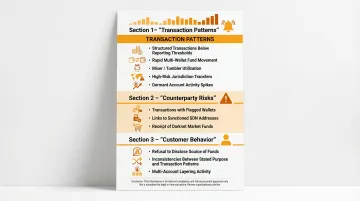

AML programs must monitor for these core transactional and behavioral red flags:

Transaction Patterns:

- Transactions structured just below regulatory reporting thresholds (smurfing)

- Rapid movement of funds across multiple wallets or chains with no business rationale

- Use of mixers, tumblers, or privacy coins to obscure trails

- Transfers to or from exchanges in jurisdictions with weak AML enforcement

- Dormant accounts that suddenly spike in activity or make large withdrawals

Counterparty Risks:

- Transfers to wallets flagged by blockchain analytics tools

- Interactions with sanctioned addresses on OFAC's SDN List

- Receipt of funds from darknet markets or illicit sources

Customer Behavior:

- Unwillingness to provide source-of-funds documentation

- Inconsistencies between stated business purpose and transaction patterns

- Use of multiple accounts to move funds through the same platform

Red flags don't confirm money laundering — but they trigger a legal obligation. Firms must conduct enhanced due diligence, and if suspicion remains after investigation, file a SAR within 30 days of detection. Regulators treat inaction on documented red flags as a compliance failure in its own right.

Emerging and Evolving Threats

Beyond established red flags, compliance teams are now tracking a second layer of risk: evasion methods that exploit newer technology and market structures.

AI-Generated Synthetic Identities: FinCEN issued Alert FIN-2024-Alert004 in November 2024, warning that criminals use GenAI to fabricate government-issued IDs and deepfake video to bypass KYC liveness checks.

Red flags include third-party webcam plugins during verification and metadata inconsistencies in submitted identity documents.

Money Mule Networks: Criminals recruit account holders to move illicit funds, and the resulting patterns often mirror normal customer behavior. Watch for:

- Transaction activity inconsistent with the account's established history

- Inbound funds with links to known fraud or human trafficking cases

NFT-Based Schemes: The US Treasury published its first NFT Illicit Finance Risk Assessment in May 2024, finding NFTs "highly susceptible to use in fraud and scams." Criminals launder money through purchases and sales of digital collectibles at inflated prices, often combining NFTs with other obfuscation methods.

Building a Crypto AML Compliance Function for Your Fintech

Every crypto fintech needs foundational infrastructure from day one:

Core Components:

- Formal written AML policy

- Designated MLRO or Chief Compliance Officer

- Documented risk assessment framework

- KYC and CDD procedures

- Transaction monitoring tools (including blockchain analytics)

- Clear SAR filing process

For early-stage companies: Getting the foundational structure right from day one is more valuable than building scale before compliance. Regulators do not make allowances for company size.

The Role of Technology

Transaction monitoring platforms, blockchain analytics tools, and KYC/identity verification software form the backbone of any scalable AML program. Technology alone isn't enough, though — these tools generate signals that require experienced human judgment to interpret, investigate, and act on.

Key technology categories:

- KYC/identity verification - Document verification, liveness detection, deepfake detection

- Blockchain analytics - Wallet risk scoring, fund flow tracing, exposure to sanctioned addresses

- Transaction monitoring - Rule-based alerts, behavioral anomaly detection, threshold monitoring

- Travel Rule infrastructure - Data sharing protocols for originator/beneficiary information exchange

Technology sets the floor. The people you hire determine the ceiling.

The People Dimension

As crypto AML requirements grow more complex, fintechs and crypto companies are competing for a limited pool of qualified AML professionals:

- Financial Crime Analysts

- BSA Officers

- Compliance Managers

- MLROs with digital asset experience

Without the right people in place early, even well-designed programs break down under alert volume, regulatory scrutiny, or enforcement action. Companies need professionals who understand both traditional AML frameworks and crypto-specific risks — mixers, chain-hopping, and Travel Rule implementation among them.

Wayoh places AML and Financial Crime professionals at crypto, fintech, and banking firms — with 10+ years in the market and 500+ professionals placed across Compliance, Risk, and Legal. For companies building or scaling a compliance function, a recruiter who knows the regulatory landscape and has access to qualified crypto compliance talent can cut time-to-hire significantly. Reach out at hiring@wayoh.co to discuss your hiring needs.

Frequently Asked Questions

What is AML compliance for crypto?

AML compliance for crypto refers to the set of laws, regulations, and internal controls that cryptocurrency companies and VASPs must implement to detect, prevent, and report money laundering and other illicit financial activity on their platforms. This includes KYC verification, transaction monitoring, Travel Rule implementation, and SAR filing.

Can cryptocurrencies be used in money laundering?

Yes, crypto has been used for money laundering due to its pseudonymity, cross-border speed, and limited centralized oversight. However, blockchain transparency and increasingly robust AML frameworks have made crypto significantly harder for criminals to exploit undetected compared to traditional cash laundering.

What does KYC have to do with AML in crypto?

KYC (Know Your Customer) is a core component of AML: it is the process through which crypto fintechs verify user identities, assess customer risk levels, and establish the baseline information needed for effective ongoing transaction monitoring and suspicious activity detection.

What is the Travel Rule and how does it apply to crypto?

The FATF Travel Rule requires VASPs to collect, verify, and pass along originator and beneficiary information for crypto transfers above a set threshold (USD/EUR 1,000 for FATF; EUR 0 for EU; $3,000 for US). This extends to digital assets the same transparency standards that apply to wire transfers in traditional banking.

Which US laws govern AML compliance for crypto companies?

The Bank Secrecy Act (BSA) is the primary framework, requiring FinCEN MSB registration for crypto firms. The GENIUS Act (2025) extended those obligations to stablecoin issuers. OFAC sanctions screening and state laws like New York's BitLicense add further compliance layers.

What happens if a crypto company fails to comply with AML regulations?

The consequences range from massive fines to criminal charges. Binance paid $4.3 billion and OKX paid $504.7 million in penalties; Binance CEO Changpeng Zhao served four months in prison for BSA violations. Non-compliance also risks license revocation and lasting reputational damage.