Introduction

In October 2024, FinCEN levied a $1.3 billion penalty against TD Bank—the largest civil enforcement action against a depository institution in U.S. Treasury history. The bank had failed to monitor trillions of dollars in transactions annually and missed $1.5 billion in suspicious activity reporting, allowing over $400 million in money laundering transactions to flow undetected. The total settlement, coordinated across FinCEN, DOJ, and the OCC, reached $3.09 billion. TD Bank became the first bank to plead guilty to conspiracy to commit money laundering, and regulators imposed a four-year independent monitorship.

That penalty exposed what many compliance leaders already know: manual KYC and AML processes cannot keep pace with modern financial crime. Financial institutions face a $61 billion annual compliance burden in the U.S. and Canada alone, yet 95% of AML alerts are false positives—each consuming up to 22 hours of investigation time.

The scale of the problem is sobering. Illicit financial flows total $4.4 trillion globally, a figure that dwarfs the detection capacity of systems still relying on manual review.

This guide is written for compliance officers, financial crime analysts, risk leaders, and banking operations teams at community banks, commercial banks, digital banks, and FinTechs navigating the shift to automated KYC and AML.

Inside: how automation works, the technologies driving it, what separates successful programs from costly failures, and how human expertise fits within these systems.

TL;DR

- KYC verifies customer identity; AML detects financial crime by combining that data with transaction monitoring

- Automation uses AI, OCR, and machine learning to handle both processes faster and with greater accuracy

- Manual processes cost $60 million annually per bank, take up to 100 days for onboarding, and produce 95% false positive rates

- Automation shifts compliance professionals from document processing to high-value investigation, escalation, and model oversight

- Success requires data quality, risk-based workflows, regulatory transparency, and compliance talent to govern automated systems

- Perpetual KYC (pKYC) enables continuous real-time monitoring—cutting operating costs by 60-80% compared to periodic review cycles

What Is KYC and AML Automation and Why It Matters for Banking Teams

KYC (Know Your Customer) is the process financial institutions use to verify customer identity, assess risk at onboarding, and maintain accurate customer profiles. It includes Customer Identification Programs (CIP), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD) for higher-risk customers. KYC establishes the foundation of who your customer is and what level of financial crime risk they represent.

AML (Anti-Money Laundering) is the broader regulatory and operational framework that uses KYC outputs to detect and prevent money laundering and terrorist financing. It draws on the Bank Secrecy Act, USA PATRIOT Act, and FinCEN guidance, and encompasses transaction monitoring, sanctions screening, and Suspicious Activity Report (SAR) filing.

KYC and AML are distinct but inseparable. KYC provides the identity and risk data that feeds the AML program; without accurate customer profiles and risk assessments, transaction monitoring systems generate excessive false positives and miss genuine threats.

Automation replaces manual document collection, data entry, and review steps with technology-driven workflows that execute checks in seconds, apply consistent logic, and generate auditable records automatically.

Instead of compliance analysts typing passport data from scanned images or manually searching sanctions lists, automated systems use OCR, AI-driven validation, biometric verification, and real-time API screening to process customers from submission to approval. Low-risk cases move straight through; high-risk cases route to human review.

The Business Case for Automation

Banking teams cannot defer automation. The numbers tell the story:

- Banks spend an average of $60 million annually on KYC compliance, with large institutions onboarding thousands of clients spending up to $30 million on KYC alone

- Corporate client onboarding takes up to 100 days, with more than 40% of that time consumed by KYC due diligence

- 89% of corporate treasurers reported a "bad experience" with KYC processes, and 13% changed banks as a result

- Global AML compliance costs exceed $274 billion annually, yet enforcement fines for AML failures have totaled $45.68 billion cumulatively since 2000

Meanwhile, the UNODC estimates 2-5% of global GDP—$800 billion to $2 trillion—is laundered annually, with illicit financial activity surging to $4.4 trillion in 2026. At that volume, manual compliance programs don't just struggle to keep up—they create blind spots that automated detection is specifically designed to close.

How KYC and AML Automation Works: Technologies and Process Flow

Automated KYC/AML operates as a continuous loop, not a one-time checkpoint. A customer enters through digital onboarding, their identity is verified, risk is scored against watchlists, and the account activates — then ongoing monitoring re-evaluates that risk in real time as behavior changes.

Step 1: Digital Identity Capture and Document Verification

Optical Character Recognition (OCR) and AI-powered document validation extract data from passports, driver's licenses, utility bills, and corporate formation documents. Modern OCR reads Machine Readable Zones (MRZ) on passports, analyzes security features like holograms and microprinting, and flags potential document fraud by comparing submitted images against known templates.

This eliminates manual data entry errors—where a compliance analyst misreads a date of birth or misspells a name—and compresses processing time from hours to seconds. AI models trained on millions of legitimate and fraudulent documents can detect alterations, deepfakes, and synthetic identity attempts that human reviewers would miss.

Step 2: Biometric Verification and Liveness Detection

Facial recognition technology matches a customer's live selfie against the photo on their submitted ID document, confirming that the person submitting the application is the genuine document owner. Liveness detection uses motion-based challenges—such as asking the user to blink, turn their head, or follow an on-screen prompt—to prevent fraudsters from submitting photos of photos or pre-recorded videos.

This step prevents identity theft and synthetic identity fraud at onboarding — particularly critical for digital banks and FinTechs that verify customers remotely.

Step 3: Automated Sanctions, PEP, and Adverse Media Screening

Real-time automated screening checks customer names against sanctions lists (OFAC, UN, country-specific watchlists), Politically Exposed Persons (PEP) databases, and adverse media sources. Global compliance requires screening against 100+ sanctions and watchlists, with OFAC's Specially Designated Nationals (SDN) list alone containing entries with 15-20 aliases each and updated 3-4 times per week.

Manual screening can't keep pace with list update frequency or name variation complexity. Automated systems run fuzzy name-matching that accounts for spelling differences, transliteration, and cultural naming conventions — flagging likely matches for analyst review and clearing obvious non-matches instantly.

Automated screening produces an auditable record regulators expect: timestamped checks, match scores, analyst decisions, and evidence of periodic rescreening as lists update. However, false positive rates remain high—often exceeding 90%—which is why tuning and intelligent workflows matter.

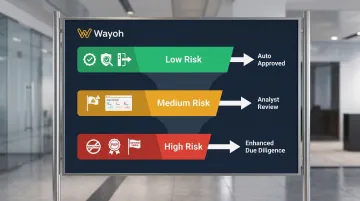

Step 4: Risk-Based Routing and Perpetual KYC (pKYC)

Machine learning models assign risk scores based on customer attributes — geography, industry, transaction patterns, PEP status — and route cases accordingly. Low-risk retail customers with verified identity and clean screening results proceed to straight-through processing.

High-risk customers flagged for sanctions proximity, adverse media, or unusual business structures are automatically escalated to Enhanced Due Diligence (EDD) queues, where analysts gather additional documentation and make approval decisions.

Perpetual KYC (pKYC) shifts KYC from periodic to continuous. Traditional KYC relies on calendar-driven reviews — annually or biannually — where compliance teams revisit customer files on a fixed schedule regardless of whether risk has changed.

pKYC re-evaluates customer risk automatically when material changes occur: a business address moves to a high-risk jurisdiction, a customer appears in new adverse media, transaction volume spikes, or they're newly designated as a PEP. PwC estimates pKYC can reduce KYC operating costs by 60-80%, saving a medium-sized bank approximately $14.4 million annually for corporate customers and $13.2 million for retail.

Trigger-based reviews replace costly calendar-driven backlogs, ensuring compliance teams focus on accounts where risk has actually changed rather than reviewing thousands of static, low-risk profiles annually.

Building a KYC/AML Automation Program: Key Success Factors

A KYC/AML automation program requires planning, governance, and talent — not just a software purchase. The institutions that succeed consistently share four traits.

Data Quality Is the Foundation

Automated systems are only as accurate as the data they process. Banks with fragmented customer data across legacy CRM systems, core banking platforms, and compliance databases will produce unreliable risk scores, duplicate records, and false positives that undermine efficiency.

Before automation can function reliably, institutions must:

- Audit customer data for completeness, accuracy, and consistency

- Remediate duplicates, incomplete profiles, and conflicting records

- Establish ongoing data governance to maintain quality as records update

- Ensure data lineage is documented so AI models can be validated and explained

Data quality directly affects AI model accuracy. If your training data contains errors — such as incorrectly labeled high-risk customers or incomplete transaction histories — your model will inherit those flaws and replicate them at scale.

Risk-Based Workflow Design Determines Operational Efficiency

Automation should not apply the same level of scrutiny to every customer. Institutions must define tiered workflows aligned to their risk appetite:

- Low-risk customers (verified identity, clean screening, stable jurisdiction, predictable transaction patterns) → straight-through processing with automated approval

- Medium-risk customers (minor screening alerts, moderate transaction complexity) → routed to simplified review with pre-populated case summaries

- High-risk customers (sanctions proximity, PEP status, adverse media, high-risk jurisdictions) → escalated to Enhanced Due Diligence with full analyst investigation

Risk-based design ensures compliance resources are allocated where they add the most value. When every case triggers manual review, the program produces overhead without the efficiency gains automation is supposed to deliver.

Explainability and Regulatory Transparency Are Non-Negotiable

Regulators expect institutions to demonstrate how automated decisions are made. AI models used for risk scoring and transaction monitoring must be interpretable, auditable, and tested regularly.

The December 2018 Joint Statement from FinCEN, OCC, FDIC, Fed, and NCUA explicitly encourages AI and digital identity technologies in BSA/AML compliance and protects pilot programs from supervisory criticism — even if unsuccessful. However, regulators require that institutions maintain effective BSA/AML programs and can explain how AI-driven risk decisions function.

Under SR 11-7 Model Risk Management guidance, institutions must:

- Validate models before production deployment and periodically thereafter (typically annually)

- Document why a complex AI model was chosen over simpler alternatives

- Implement explainability techniques (SHAP, LIME) to interpret model outputs

- Monitor for model drift monthly (or more frequently for high-risk models)

- Define "material change" thresholds that trigger re-validation

Regulators don't just want to see that automation is working — they want to see that your team understands why it made each decision. That distinction determines whether your program survives an exam.

Technology Integration Into Core Banking Infrastructure Takes Planning

KYC/AML automation tools must connect via APIs to CRM systems, core banking platforms, case management tools, and compliance databases. Poor integration creates data silos rather than eliminating them.

The result: compliance analysts toggling between systems, re-entering data manually, and reconciling conflicting records — exactly the inefficiencies automation was supposed to solve.

Common integration failure points include:

- Real-time screening APIs that don't update case management systems automatically

- OCR platforms that extract data but don't populate customer profiles in core banking

- Risk scoring models that run in standalone environments without feeding decisioning workflows

- Transaction monitoring alerts that generate in one system while customer profiles live in another

Before go-live, map every data flow end-to-end, document API dependencies explicitly, and run integration tests across all connected systems — not just the components in isolation.

Common Misconceptions and Limitations of KYC/AML Automation

Misconception: Automation Means Full Autonomy

Current AI systems, even agentic ones, require human oversight for escalations, edge cases, model validation, and final decision-making on high-risk cases. Institutions that eliminate compliance headcount entirely after automation often create regulatory exposure.

A compliance analyst's role shifts from document processing to investigation, exception handling, and model governance—but it does not disappear. The TD Bank enforcement action demonstrates what happens when institutions allow AML programs to "languish" without adequate human oversight, even when technology is in place.

Misconception: Automation Solves Compliance

Technology replaces manual steps but does not replace compliance judgment. Institutions must still interpret regulations, respond to regulatory inquiries, design risk frameworks, and make defensible decisions.

Effective KYC/AML programs require compliance leadership who can:

- Interpret regulatory expectations and translate them into operational controls

- Communicate risk decisions clearly to senior management and examiners

- Maintain meaningful oversight of automated systems

Automation supports these activities. It does not replace the judgment behind them.

Limitation: False Positive Fatigue and Model Drift

ML-based transaction monitoring can generate high volumes of false positives without proper tuning. An estimated 95% of alerts from traditional AML systems are false positives, with each alert requiring up to 22 hours of investigation. AI-enabled screening can reduce false positives by 20-60%, but even a 50% reduction still leaves substantial workloads.

Model drift occurs when AI models trained on historical data become less effective as criminal typologies evolve. Fraudsters adapt; models trained on yesterday's patterns miss tomorrow's schemes. Continuous testing, recalibration, and feedback loops are required to maintain accuracy.

Institutions should build monitoring cadences that match the risk profile of each model:

- Monthly monitoring as a baseline for standard models

- Weekly or daily monitoring for high-risk or high-volume models

- Automated drift alerting using tools like the Kolmogorov-Smirnov test or Population Stability Index to flag performance degradation before it creates compliance gaps

The Human Element: Compliance Talent in an Automated World

As automation reshapes compliance workflows, the skill profile of compliance professionals must evolve. Teams need people who understand how automated systems work, can interpret model outputs, manage exception queues, validate AI decisions, and engage regulators on technology-driven programs—not just those who can process documents manually.

The Roles That Matter Most in Automated Environments

- AML Investigators: Analyze escalated alerts, conduct enhanced due diligence, determine SAR filing thresholds, and document investigative findings

- Transaction Monitoring Analysts: Tune rule parameters, review system alerts, clear false positives, and escalate genuine threats

- KYC QC Reviewers: Validate automated identity verification and risk scoring, audit sample cases, and confirm CDD/EDD compliance

- Compliance Technology Managers: Oversee platform integrations, coordinate model validation, and bridge compliance and technology teams

- BSA/AML Officers: Communicate AI-driven risk decisions to regulators and leadership, design risk-based workflows, and maintain program governance

The talent crisis intensifies the need for automation. 99% of financial crime departments struggle to find qualified talent, and 86% of compliance professionals report their department is understaffed. Technology-related roles now account for 52% of all financial crime compliance recruitment costs, up from 34% in 2022.

For banking and FinTech teams building or scaling a KYC/AML automation program, staffing the right people alongside the right technology is what separates programs that pass regulatory scrutiny from those that don't.

Wayoh has spent 10+ years placing BSA officers, AML investigators, transaction monitoring analysts, and compliance technology managers at community banks, commercial banks, and FinTechs. If you're building a team to govern an automated compliance program, reach out to Wayoh to find the right people for it.

Conclusion

KYC and AML automation is no longer optional for banking teams—it is the mechanism through which institutions meet regulatory expectations, protect customers, reduce costs, and compete. Its value, though, depends entirely on how well it is designed, governed, and staffed—technology without the right people behind it delivers compliance theater, not compliance.

As AI capabilities advance from analytical to agentic, regulatory expectations around real-time monitoring and explainability are rising in parallel. Institutions that invest now in both automation infrastructure and experienced compliance talent—AML analysts, BSA officers, and financial crime specialists who can govern these systems—will be best positioned to manage financial crime without sacrificing customer experience or regulatory standing.

The TD Bank enforcement action is the clearest recent example of what inadequate programs cost: $3 billion in penalties and a growth cap that will define the bank for years. Regulators have shown they will act. The institutions that treat compliance hiring as a strategic priority—not a backfill exercise—are the ones that won't be next.

Frequently Asked Questions

What is the relationship between AML and KYC?

KYC is the identity verification and risk assessment process that forms the foundation of any AML program. AML is the broader regulatory and operational framework that uses KYC data alongside transaction monitoring, screening, and suspicious activity reporting to detect and prevent financial crime. They are distinct but inseparable—effective AML requires accurate KYC.

What are the 4 pillars of AML KYC?

The four pillars are: Customer Identification Program (CIP), Customer Due Diligence (CDD), Enhanced Due Diligence (EDD), and Ongoing Monitoring. Automation supports each one — from OCR-driven identity capture at onboarding to perpetual KYC systems that flag risk changes in real time.

What is perpetual KYC (pKYC) and how is it different from traditional KYC?

Traditional KYC runs on a fixed calendar schedule (annually or biannually). pKYC monitors customer behavior and data continuously, triggering reviews automatically when material risk changes occur — such as moves to high-risk jurisdictions or new adverse media hits. The result is more accurate risk profiles and fewer compliance backlogs.

What technologies are most commonly used in KYC automation?

The most widely used technologies include:

- OCR for document data extraction

- AI and machine learning for document validation and risk scoring

- Biometric verification and liveness detection for identity confirmation

- Robotic process automation (RPA) for repetitive workflow tasks

- Real-time screening APIs for sanctions and PEP checks

Can KYC and AML processes be fully automated without human review?

Automation handles the majority of routine checks, but human review remains essential for high-risk cases, regulatory escalations, model oversight, and decisions requiring contextual judgment. Running fully automated programs without human oversight creates regulatory risk — regulators expect institutions to maintain clear governance over automated decisions.

How do regulators view AI-driven KYC and AML compliance programs?

U.S. regulators including FinCEN and bank supervisory agencies support the use of technology in compliance but require that AI-driven decisions be explainable, auditable, and subject to human oversight. Institutions should engage regulators early when implementing significant automation changes. Transparent documentation of how models function is a baseline expectation, not optional.