Introduction

Neobanks face a fundamental paradox: the very features that make them innovative—instant onboarding, 24/7 accessibility, frictionless digital account opening—are the same characteristics that expose them to financial crime. Remote identity verification, high-velocity customer acquisition, and real-time payment rails create vulnerabilities that traditional banks with physical branches simply don't face.

This digital-first model has drawn intensifying regulatory scrutiny, with enforcement actions highlighting a pattern of compliance breakdowns across the sector.

Global neobanking revenue is projected to surge from $211.20 billion in 2025 to $9,384.73 billion by 2033, a 61.9% compound annual growth rate. As transaction volumes climb and customer bases scale, regulators are paying close attention.

What many neobanks underestimate: AML compliance is ultimately a people problem, not just a technology problem. Your transaction monitoring platform matters, but the licensed professionals on your banking security team determine whether your program holds up to a regulatory examination or breaks down under scrutiny the way Robinhood's did.

This article breaks down how to build and staff the AML compliance function that keeps pace with neobank growth without inviting regulatory intervention.

TLDR

- Neobanks' instant onboarding and real-time payments create unique financial crime exposure that regulators are actively scrutinizing

- AML pillars like CDD/KYC, transaction monitoring, and SAR filing require trained staff — documented policies alone won't satisfy regulators

- Enforcement actions repeatedly cite inadequate staffing as root cause, with penalties reaching $30 million for compliance failures

- Build your AML team around a BSA Officer, AML Analysts, KYC Specialists, and Financial Crime Investigators — scaled to your growth stage

- Credentialed AML professionals are passive candidates requiring network-first recruiting, not generic job postings

Why Neobanks Are Uniquely Exposed to Financial Crime Risk

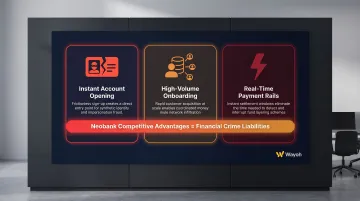

Neobanks' defining competitive advantages become liabilities in the hands of sophisticated criminals. The same features that drive customer growth create three distinct financial crime openings:

- Instant account opening without physical document verification makes identity theft and synthetic identity fraud easier to execute at scale

- High-volume onboarding that prioritizes speed over thoroughness gives money mule networks room to establish accounts in bulk

- Real-time payment rails—including SEPA Instant Credit Transfer and, increasingly, the US RTP network and FedNow—enable rapid layering of illicit funds before detection systems can respond

The scale of exposure compounds these risks. According to Statista data, global neobanking transaction value reached $3.34 trillion in 2022, with an 18.16% CAGR projected through 2027. That growth creates relentless operational pressure: neobanks face a genuine tension between onboarding customers at speed and conducting thorough due diligence. Many choose speed and accept the risk.

Regulators have taken notice. FATF explicitly identifies instant payment methods and new payment technologies as higher-risk channels for money laundering and terrorist financing, citing the significant rise in transaction volumes through internet and mobile payments. The problem crosses jurisdictions. Under the EU Instant Payments Regulation, transaction screening windows can be as brief as 10 seconds — a constraint that US neobanks operating on RTP and FedNow rails are beginning to face as well.

Enforcement actions validate these concerns. The UK Financial Conduct Authority fined Starling Bank £29 million in 2024 for financial crime control failures, including opening more than 54,000 accounts for 49,000 high-risk customers while sanctions screening measures failed to keep pace with growth. Digital onboarding at scale, without proportionate compliance infrastructure, draws regulatory consequences — a lesson US neobanks cannot afford to ignore.

The 4 Pillars of AML Compliance Every Neobank Must Execute

Customer Due Diligence (CDD) and KYC

Under 31 CFR 1020.210, banks must implement risk-based procedures for ongoing customer due diligence, including understanding the nature and purpose of customer relationships to develop risk profiles. For neobanks, this obligation translates into remote identity verification using:

- Biometric authentication (facial recognition, liveness detection)

- Digital document verification (passport, driver's license scanning)

- Database checks (credit bureaus, watchlists, adverse media screening)

- Beneficial ownership identification for business accounts (25% ownership threshold under the CDD Final Rule)

Enhanced due diligence applies to higher-risk customers: Politically Exposed Persons (PEPs), customers in high-risk jurisdictions, and cross-border clients. KYC is the onboarding component within the broader CDD obligation. It covers initial verification; CDD extends that obligation through ongoing monitoring and updating of customer information across the full relationship.

Transaction Monitoring

Neobanks must continuously monitor account activity for suspicious patterns including unusual transfer volumes, structuring behavior (breaking large transactions into smaller amounts to avoid reporting thresholds), high-risk merchant activity, and rapid cross-border fund movement. This requires automated systems configured to detect anomalies relative to customer profiles.

The challenge intensifies on real-time payment networks. Under EU regulations, payment service providers must screen customer databases daily and upon sanctions list updates. However, transactional screening for EU targeted financial sanctions in instant credit transfers is prohibited to meet the 10-second processing requirement.

The practical consequence: neobanks must front-load screening into onboarding and rely on pre-transaction, customer-level controls. It's a workable model, but a higher-risk one.

Suspicious Activity Reporting (SAR/STR)

Under 31 CFR 1020.320, banks must file Suspicious Activity Reports when they know, suspect, or have reason to suspect illegal activity, BSA evasion, or transactions with no apparent lawful purpose. Key SAR requirements:

- Filing threshold: Transactions involving or aggregating at least $5,000

- Deadline: No later than 30 calendar days after initial detection (extendable to 60 days only if no suspect is identified)

- Retention: SAR copies and supporting documentation must be kept for five years from the filing date

One thing automated systems can't do: make the filing decision. Algorithms flag suspicious activity, but trained compliance professionals assess context, investigate, and determine whether the activity clears the legal threshold for reporting.

AML Program Governance and Training

31 U.S.C. 5318(h)(1) requires banks to establish AML programs that include, at minimum:

- Written internal policies and procedures

- A designated AML Compliance Officer responsible for day-to-day compliance coordination

- Ongoing employee training appropriate to roles

- Independent audit function to test the program

Regulators assess the quality of this governance structure during examinations. A documented policy that sits on a shelf while actual operations run differently is worse than no policy at all—it demonstrates awareness of requirements coupled with willful failure to implement them.

Five Classic Red Flags in AML:

Compliance staff must be trained to recognize:

- Structuring/smurfing - Breaking transactions into amounts below reporting thresholds

- Unusual activity inconsistent with customer profile - A student account suddenly moving $500,000

- Rapid layering - Funds moving quickly through multiple accounts to obscure origin

- High-risk jurisdiction involvement - Transactions to/from jurisdictions with weak AML controls

- Customer reluctance to provide information - Evasive answers about business purpose or fund sources

How Understaffing Causes Compliance Failures—And What It Costs

In August 2022, the New York Department of Financial Services imposed a $30 million penalty on Robinhood Crypto for significant BSA/AML violations. The findings were damning: transaction monitoring failures, improper certifications to regulators, massive alert backlogs, and—most tellingly—explicit citation of insufficient BSA/AML staffing relative to the company's explosive growth. The regulator's message was clear: you cannot automate your way out of AML obligations. Technology without trained human oversight is not a compliance program.

Robinhood is not alone. BaFin ordered N26 Bank to limit customer growth to 50,000 new customers per month in November 2021 and installed a special commissioner due to shortcomings in risk management tied to substantial growth. In May 2024, BaFin imposed a €9.2 million fine on N26 for systematically late suspicious activity reports. The pattern repeats: prioritizing onboarding speed over compliance thoroughness—a staffing and process failure—creates regulatory exposure.

Reactive compliance hiring costs far more than building proactively. Rebuilding a program after an enforcement action means recruiting senior, expensive talent under a consent order—on tight deadlines and under public scrutiny. The financial exposure extends well beyond fines:

- Independent compliance monitors, whose fees can reach hundreds of thousands of dollars annually

- Transaction lookback reviews spanning multiple years of activity

- Enhanced reporting requirements that consume staff time indefinitely

Emergency remediation hiring is the most expensive form of compliance investment. Strategic team building before a problem surfaces is the only cost-effective alternative.

Key AML Roles to Build on a Neobank Banking Security Team

BSA/AML Compliance Officer

This is a legally mandated role under 31 U.S.C. 5318(h)(1). The BSA Officer is responsible for:

- Owning the AML program end-to-end

- Interfacing with regulators during examinations

- Overseeing all SAR filings

- Managing the compliance calendar (audits, training, policy updates)

- Serving as the organization's primary regulatory point of contact

For early-stage neobanks, this person may also function as the Chief Compliance Officer or even CISO, wearing multiple hats. As the platform scales beyond Series A, these roles should separate—BSA/AML requires dedicated focus, and splitting attention across information security, consumer compliance, and financial crime creates gaps.

AML Analyst / Financial Crime Analyst

This is typically the highest-volume role on the team. Analysts review transaction monitoring alerts, investigate flagged activity, document findings, and make SAR filing recommendations. The quality of your analyst team directly determines whether your monitoring system operates effectively or drowns in false positives that mask genuine threats.

Analysts need regulatory knowledge, investigative discipline, and the ability to synthesize transaction patterns into coherent narratives. A weak analyst will close alerts without sufficient investigation; a strong analyst will identify the money mule network operating across 15 accounts that a superficial review would miss.

KYC / Customer Due Diligence Specialist

KYC Specialists focus on onboarding-stage verification: validating customer-submitted documents, conducting enhanced due diligence reviews for flagged customers, collecting beneficial ownership information for business accounts, and managing ongoing periodic reviews required under CDD regulations.

This role requires regulatory knowledge and strong judgment, not just process execution. A KYC Specialist must recognize when a seemingly legitimate business structure is actually a shell company designed to obscure beneficial ownership, or when document inconsistencies indicate synthetic identity fraud.

Financial Crime Investigator

Investigators handle complex cases involving potential SAR filing, working cross-functionally with legal counsel, fraud teams, and law enforcement liaisons when appropriate. Unlike analysts who review routine alerts, investigators dig into sophisticated schemes: trade-based money laundering, funnel account networks, or structuring operations spanning multiple jurisdictions.

This role requires deeper experience with money laundering typologies specific to digital banking environments. Former law enforcement, Financial Intelligence Unit (FIU) professionals, or senior bank investigators bring the pattern recognition and investigative depth this role demands.

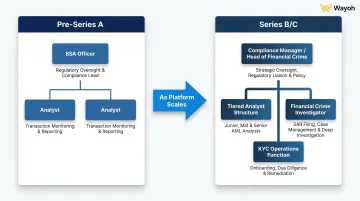

Team Scaling by Stage

Pre-Series A: A single senior BSA Officer may cover multiple functions with one or two analyst-level support staff. The BSA Officer handles program management, regulatory reporting, and high-level investigations while analysts manage routine alert review.

Series B/C: Teams typically need:

- A dedicated Compliance Manager or Head of Financial Crime

- A tiered analyst structure (junior analysts on straightforward alerts, senior analysts on complex cases)

- A dedicated KYC operations function handling onboarding reviews

- At least one Financial Crime Investigator for SAR-level cases

The ratio of compliance staff to customer base varies widely by business model, transaction volume, and risk profile, but chronic understaffing is the most common failure mode. Building that infrastructure before regulators force the issue is far cheaper than reconstructing it under a consent order—enforcement actions routinely run into seven-figure remediation costs before the fines even start.

Skills and Credentials to Prioritize When Evaluating AML Candidates

Certifications That Signal Credentialed Expertise

CAMS (Certified Anti-Money Laundering Specialist) is the most recognized credential in the field, administered by ACAMS, the largest international membership organization for anti-financial crime professionals. CAMS certification demonstrates foundational AML knowledge and commitment to the profession. For neobanks specifically, prioritize candidates with direct BSA program management experience and familiarity with FinCEN reporting requirements, not just policy-writing or theoretical knowledge.

CFCS (Certified Financial Crime Specialist) is a cross-disciplinary credential covering AML, fraud, and sanctions. While less common than CAMS, CFCS holders often bring a broader financial crime perspective that maps well to neobank environments where fraud and AML risks overlap.

Certifications alone don't guarantee job readiness. A candidate with CAMS but no hands-on SAR filing experience or regulatory examination participation will struggle in a neobank environment where regulatory scrutiny is intense and tolerance for learning curves is low.

Neobank or FinTech Experience Versus Traditional Banking Experience

There's a real trade-off between the two candidate pools:

Traditional bank compliance professionals bring:

- Structured BSA program knowledge and formal examination experience

- Understanding of regulatory expectations and examiner documentation standards

- Depth in policy development and audit-ready record-keeping

FinTech-native compliance professionals bring:

- Comfort with digital onboarding tools and API-driven verification systems

- Ability to work alongside engineering and product teams at startup speed

- Familiarity with how compliance integrates into rapid product iteration

The strongest AML hires bridge both worlds: professionals with traditional bank compliance foundations who have transitioned into digital banking environments and kept their regulatory rigor intact.

Technical and Platform Fluency

AML roles at neobanks require more than compliance knowledge — candidates need hands-on technical capability. Look for comfort with transaction monitoring platforms such as Actimize, NICE, or in-house tools, along with the following:

- SQL querying: Ability to pull transaction data, validate alert accuracy, and conduct investigative research beyond what the monitoring system surfaces

- Rule set tuning: Experience adjusting thresholds, calibrating scenarios, and reducing false positive rates without creating blind spots

- System adaptability: Willingness to learn proprietary or evolving monitoring tools as the neobank's infrastructure scales

Candidates who can only operate within pre-configured systems will hit a ceiling fast — and drag the compliance program with them as transaction volumes and product complexity grow.

Hiring Strategies for Specialized AML Talent in the Neobank Space

Understand That Credentialed AML Professionals Are a Constrained Talent Pool

The intersection of BSA/AML expertise and neobank-specific experience is narrow. Most senior AML professionals—those with CAMS certification, multiple years of SAR filing experience, and regulatory examination track records—are passive candidates. They are employed, not actively job-searching, which means generic job board postings will surface junior or mismatched candidates while the people you actually need remain invisible.

According to the Bureau of Labor Statistics, compliance officers across all industries earned a median annual wage of $78,420 in May 2024, with employment of 418,000 and just 3% projected growth through 2034. The competition for experienced AML talent is intense, and neobanks compete against established banks with larger compensation budgets and less regulatory risk.

Prioritize Network-First Sourcing Over Keyword-Matching

The highest-quality AML and financial crime professionals are typically hired through direct referrals, community relationships, and recruiters who have maintained ongoing dialogue with candidates over years—not through resume databases or LinkedIn keyword searches. This is especially true for roles like BSA Officer or Financial Crime Investigator, where regulatory accountability is personal.

A BSA Officer's name appears on regulatory filings; their professional reputation is tied directly to program quality. These professionals move carefully and rely on trusted networks when considering new opportunities.

Network-first sourcing means activating personal connections before posting anything publicly. In practice, that looks like:

- Knowing who the experienced AML professionals are in your region and what motivates them

- Understanding their career history and who they've worked alongside

- Engaging recruiters who have spent years in the compliance community, not algorithms matching keywords

Speed and Confidentiality Matter in Compliance Hiring

Compliance team gaps are not neutral—they represent live regulatory exposure. An unfilled BSA Officer position means someone else is covering those responsibilities inadequately or not at all. A backlog of unreviewed transaction monitoring alerts accumulates while you're conducting a four-month hiring process with multiple panel interviews and slow decision-making.

For AML roles specifically, a slow hiring process isn't just inefficient—it leaves a neobank running a weakened compliance function for months. The right hiring partner should:

- Mobilize quickly and present qualified candidates within weeks, not months

- Operate with discretion throughout the search

- Protect confidentiality, since visible signals of compliance team turnover can prompt regulatory questions

Wayoh's Approach to Neobank AML and Financial Crime Hiring

For neobanks building or scaling AML and financial crime teams, Wayoh brings 10+ years of specialized focus in Banking and FinTech compliance hiring. The firm's network is built through real relationships with BSA Officers, AML Analysts, KYC Specialists, and Financial Crime Investigators—not resume database scraping or keyword matching.

Wayoh's team understands the regulatory landscape, knows what examiners expect, and identifies candidates with both technical AML expertise and the adaptability neobank environments demand. The process is consultative and built for speed, without sacrificing the rigor that compliance hiring requires.

Frequently Asked Questions

What are the 4 pillars of AML compliance?

The four pillars are:

- Customer Due Diligence (CDD/KYC) — verifying identities and assessing risk profiles

- Transaction Monitoring — screening account activity for suspicious patterns

- Suspicious Activity Reporting (SARs) — filing reports with FinCEN when thresholds are met

- AML Program Governance — written policies, a designated compliance officer, staff training, and independent auditing

All four must be operationally active, not just documented, to pass regulatory examination.

What are the five red flags in AML?

The five classic red flags are:

- Structuring (smurfing) — splitting large transactions to stay under reporting thresholds

- Unusual activity — transactions inconsistent with the customer's stated business purpose

- Rapid layering — moving funds across multiple accounts to obscure their source

- High-risk jurisdictions — activity tied to countries with weak AML controls

- Customer reluctance — refusal to provide ID or explain the purpose of transactions

What is AML and FATCA?

AML (Anti-Money Laundering) is the regulatory framework requiring financial institutions to detect and prevent money laundering through customer screening, transaction monitoring, and suspicious activity reporting. FATCA (Foreign Account Tax Compliance Act) is a US law requiring foreign institutions to report US account holders to the IRS to prevent tax evasion. Both create compliance obligations for neobanks with cross-border customers, but each targets a distinct concern.

What is the $3,000 rule in banking?

The $3,000 rule under the Bank Secrecy Act requires financial institutions to collect and retain records for funds transfers and transmittals of funds at or above $3,000, including customer identification and transaction details. This recordkeeping obligation is separate from the $10,000 Currency Transaction Report (CTR) threshold and applies to neobanks handling peer-to-peer payments or cross-border transfers.

What certifications should I look for when hiring AML compliance professionals for a neobank?

CAMS (Certified Anti-Money Laundering Specialist) is the most widely recognized credential; CFCS (Certified Financial Crime Specialist) adds cross-disciplinary depth. For neobanks, however, hands-on experience with digital onboarding controls, transaction monitoring platforms, and SAR filing matters as much as any certification. A CAMS holder without real regulatory examination experience will be underprepared for a high-scrutiny environment.